6 Ways to Cope in Your Retirement Savings & Spending Under the Current DOGE, Tariff Regime

In this issue:

- Latest in Retirement Savings & Personal Finance: Tax Season, Regulations Relaxed, Low Housing Affordability

- 6 Ways to Cope in Your Retirement Savings & Spending Under the Current DOGE, Tariff Regime

- 401k Early Withdrawal Cost Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: Tax Season, Regulations Relaxed, Low Housing Affordability

Here is some of the latest news:

Tax Season Upon Us

- For most individuals in the U.S., the tax filing deadline is Tuesday, April 15, 2025.

- There are many tax software to consider, in addition to the gold standard of Turbotax: here is a table from cnet:

Based on CNET’s reviews of tax software for 2025, here’s a comparison table of the best options:

| Tax Software | Best For | Key Features |

|---|---|---|

| TurboTax | Most people | – Intuitive interface – Comprehensive guidance – Industry leader |

| H&R Block | Best free experience | – Impressive user interface – Many free forms available |

| FreeTaxUSA | Free to low-cost filing | – Budget-friendly option – Comprehensive coverage |

| Cash App Taxes | Confident filers | – Completely free – Best for those comfortable with taxes |

| TaxSlayer | Freelancers and gig workers | – Specialized features for self-employed |

| TaxAct | Best accuracy guarantee | – Strong accuracy assurance |

Cryptocurrency Markets Regulations Relaxed

- Robinhood and Coinbase Investigations Dropped: The SEC closed its investigation into Robinhood Crypto without taking any enforcement action, one day after it dropped ts case against Coinbase. Both companies are cryptocurrency brokerages.

- SEC Regulation Rescinded: The SEC rescinded Staff Accounting Bulletin 121 (SAB 121), which had imposed stringent accounting requirements on institutions custodying crypto assets.

- Crypto Industry’s Increasing Political Influence: The crypto industry has spent heavily to help elect crypto-friendly lawmakers, including President Trump. Trump’s pro-crypto stance is expected to lead to new regulation in the US, potentially influencing other leading economies

Of course, we advise caution when participating in the frenzy surrounding meme coins, as they often end up harming retail investors. In our opinion, there should be no place for these so-called alternative coins in one’s retirement savings.

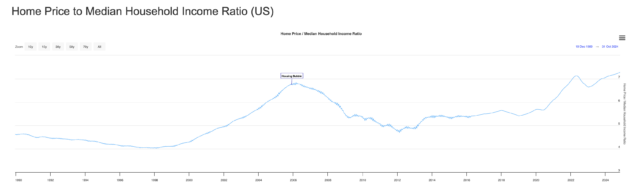

Housing Affordability Remains Historically Low

Since World War II (1946), U.S. housing affordability has reached its lowest point, as depicted in this chart:

It’s even less affordable than at the peak of the housing bubble before 2008!

6 Ways to Cope in Your Retirement Savings & Spending Under the Current DOGE, Tariff Regime

The current economic landscape, shaped by policies such as the Department of Government Efficiency (DOGE) and ongoing tariff regimes, are making almost non-stop daily news. Regardless of which side you are on, it nevertheless presents significant challenges for retirees managing their savings and spending.

1. Control Discretionary Spending Amid Rising Inflation

Tariffs are inflationary, at least in the short term. Rising inflation means retirees may need to withdraw more from their savings to cover increased living costs. To cope, focus on controlling discretionary spending by cutting back on non-essential expenses like dining out or luxury purchases. Your goal is to keep your withdrawal rate within an acceptable range.

2. Shift to Active Fixed Income Management

With inflation remaining high, interest rates may be forced to stay elevated, leading to greater volatility in fixed-income bond investments. To adapt, you can shift your bond exposure to shorter-term investments for now. Better yet, consider investing in high-quality total return bond funds, such as those from PIMCO (PIMCO Income), BlackRock, or DoubleLine. However, even these funds carry the risk of losses. To minimize significant losses, consider an actively managed rotation portfolio, such as MyPlanIQ’s total return bond fund portfolios.

3. Prepare for Stock Market Volatility

Stocks are currently expensive and may face a significant correction. Retirees should be mentally prepared for potential portfolio drawdowns. If the possibility of losses exceeds your risk tolerance, consider reallocating a portion of your investments into actively managed or defensive assets. Diversification is key to mitigating risks during market downturns. Additionally, adopting a more active tactical approach for part of your portfolio might be wise if you’re particularly concerned about investment fluctuations.

4. Budget for Rising Healthcare Costs

Even as DOGE slashes government spending, healthcare costs—a major expense for individuals—remain high and lack a concrete plan for reduction. With potential cuts to subsidies, out-of-pocket costs for drugs and care may rise. One should budget for increased healthcare expenses and explore options like supplemental insurance or health savings accounts (HSAs) to offset these costs.

5. Work Longer to Extend Savings

Working longer is an effective way to cope with rising costs and extend the longevity of retirement savings. Delaying withdrawals from retirement accounts allows them more time to grow, while additional income helps manage expenses. Staying employed, even part-time, also benefits physical and mental health, keeping retirees active and engaged.

6. Advocate for Support Systems for the Vulnerables

For those with physical or health limitations, working or working longer may not be feasible. In such cases, maintaining existing support systems like Social Security and Medicare is crucial. As Warren Buffett emphasized in his latest Berkshire Hathaway report, Just like what Buffett said in his latest Berkshire Hathaway annual report, “Take care of the many who, for no fault of their own, get the short straws in life. They deserve better”. Yes, ensuring robust policies for vulnerable populations remains essential in a wealthy nation like the U.S.

Tools & Tips: 401k Early Withdrawal Cost Calculator

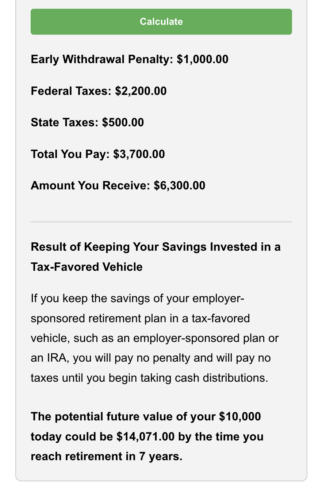

The 401(k) Early Withdrawal Cost Calculator helps you estimate the financial impact of taking an early distribution from your 401(k) or a qualified retirement plan (QRP).By entering details about your expected federal and state tax rates, retirement timeline, and anticipated annual returns, you can see both the immediate costs of an early withdrawal and the potential value of leaving your funds invested until retirement.

The inputs:

After entering the inputs, you get the following outputs:

We’ve received numerous questions about withdrawing from 401(k) accounts. We understand that many may need access to these funds. However, we strongly encourage exploring other options—such as a 401(k) loan—before making a withdrawal, which could result in penalties and reduce your future retirement savings. For more details, check the information below the calculator on this page.

Market Overview

A few developments last week on the financial and economic fronts:

- Inflation: The Consumer Price Index (CPI) report released on Wednesday showed inflation remains sticky. Core inflation, excluding volatile energy and food prices, rose at an annual rate of 3.3% in January, slightly above economists’ expectations and the previous month’s

- Consumer Spending: Retail sales data for January indicated a significant slowdown in consumer spending. Sales fell 0.9% on a seasonally adjusted basis compared to the previous month, marking the largest monthly decline in a year and falling well below economists’ expectations.

- Earnings Season: The U.S. earnings season is winding down, Factset reported that as of February 14, 2025, the blended S&P 500 earnings growth rate for the S&P 500 is 16.9% after 77% of the S&P 500 companies reported earnings results for Q4, 2024.

- European Markets: European stocks have outperformed U.S. equities so far in 2025, with a European index up more than 12% year-to-date compared to the S&P 500’s 4% gain. This might signal finally foreign stocks finally start to outperform the U.S. stocks, which have had outperformed for the past decade.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -2.0% | -1.8% | 0.1% | 7.3% | 19.0% | 4.5% |

| Foreign Stocks | -0.5% | 2.4% | 5.1% | -0.4% | 8.4% | 3.0% |

| US REITs | 0.0% | 1.0% | -3.9% | -1.6% | 12.3% | 1.6% |

| Emerging Market Stocks | 1.1% | 4.1% | 4.6% | 5.7% | 15.2% | 6.2% |

| Bonds | 0.5% | 1.3% | 0.7% | -0.3% | 5.3% | 1.5% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?