Retirement Plan Contribution Limits in 2025

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2025

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2025

Need to tap your 401(k) savings, follow the following order: Hardship Withdrawal, 401(k) Loan, and, as a last resort, a 401(k) withdrawal with penalties.

A cheat sheet for the important milestone ages such as Rule of 55, Catch-up Contributions, Medicare age,…

For individuals with multiple income streams, such as physicians, small business owners, startup founders, entrepreneurs, and consultants in tech or other fields, it’s possible to exceed the IRS’s annual limit for tax-deferred retirement savings ($69,000 for 2024 and $70,000 for 2025).

The Mega Backdoor Roth 401(k) or Mega Backdoor Roth Conversion is a powerful tool for high-income earners who want to maximize their retirement savings and enjoy tax-free withdrawals. By leveraging this strategy, you can compound your savings dramatically over time, providing significant long-term financial benefits.

We discuss the pros and cons of 401(k) brokerage link accounts

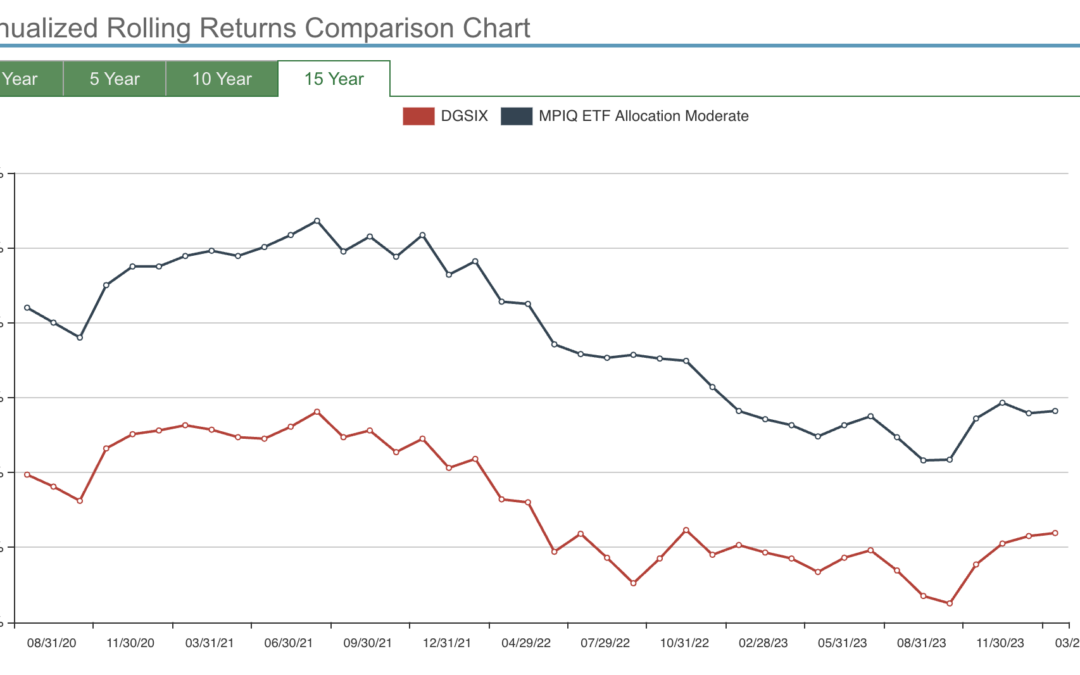

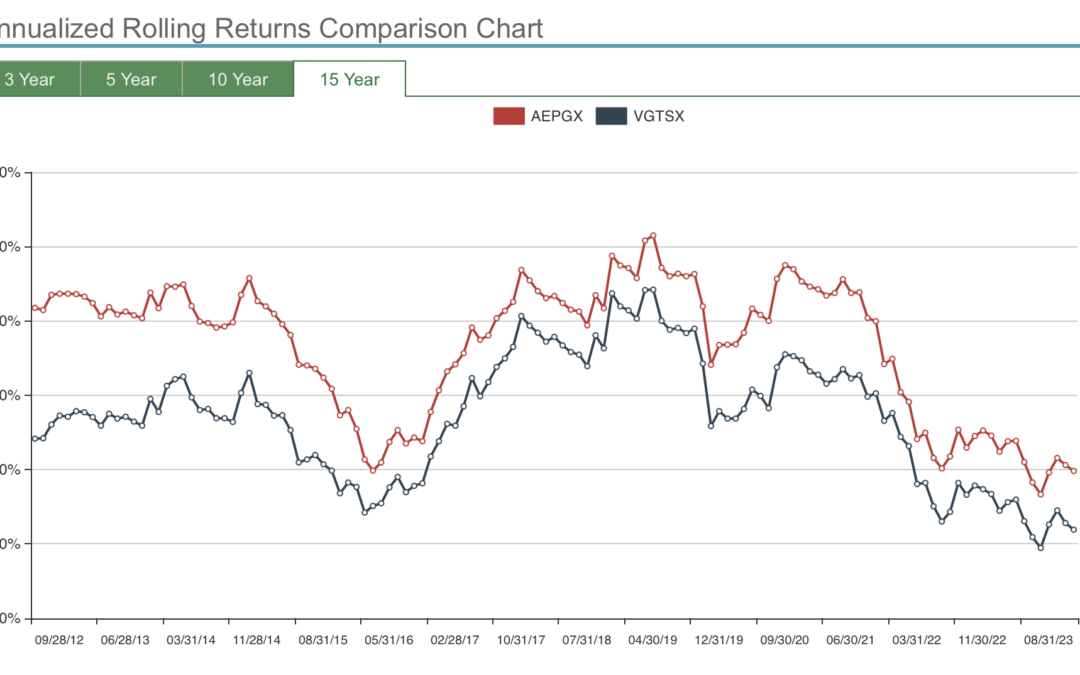

We discuss how to utilize our newly upgraded free comparison tool to better evaluate and compare ETFs, mutual funds and portfolios using rolling returns

We propose a core satellite portfolio solution to 401k accounts that have active constant new contributions.

At the current market environment, it is pertinent to explore how to adding a risk management layer to a strategic buy and hold portfolio.

The latest newsletter collection that incorporates newsletters since last update in March.

We modified several brokerage specific commission free plans to make them less bloated and easier to maintain.

High yield bonds are not necessary in asset allocation. They can be substituted with highly liquid and pure stock and Treasury indexes.

Stocks are historically weaker in summer. This is one of few prominent stock market anomalies investors should be aware to make a proper risk management decision.

Looking at historical data, one can see that in the rising rate environment from 1940-1982, stocks tended to do better while in the meantime, bonds suffered. But are we in a similar era as in those years?