IRAs as One of the Emergency Fund Sources

In this issue:

- Latest in Retirement Savings & Personal Finance: Back-and-forth Tariff Policies, Stock Market Swings, and Bond Market Stress

- IRAs as One of the Emergency Fund Sources

- The Gotcha in Maximum Solo 401(k) or SEP IRA Contribution Limits

- Market Overview

Latest in Retirement Savings & Personal Finance: Back-and-forth Tariff Policies, Stock Market Swings, and Bond Market Stress

Back-and-forth Tariff Policies

The Trump administration’s back-and-forth on tariffs created confusion. After imposing sweeping tariffs, Trump announced a 90-day suspension for many, then late Friday issued temporary exemptions for key tech imports like smartphones and chips.

Stock Market Swings

As a result, the S&P 500 recently experienced unprecedented volatility, with three record-breaking intraday swings occurring within days of each other in April 2025:

- Largest Intraday Point Swings in S&P 500 History: 532.91 points (April 9, 2025)

- Context: Triggered by President Trump’s abrupt 90-day suspension of most new tariffs.

- Impact: The S&P 500 surged 9.52% that day, marking its third-largest daily percentage gain since WWII.

- 411.53 points (April 7, 2025)

- Context: Followed Trump’s announcement of aggressive tariffs on Chinese imports.

- Significance: Nearly double the previous largest swing before April 2025.

- 357.05 points (April 8, 2025)

- Context: Continued market turbulence as investors digested tariff policies

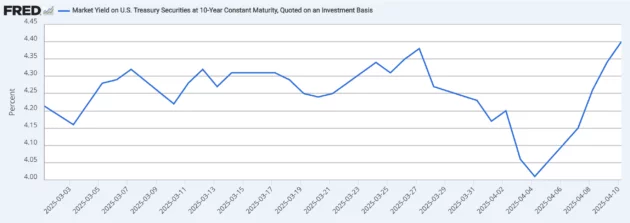

Long-Term Bond Yield Surged

Another unexpected and unusual phenomenon during this tariff period is that the 10-Year U.S. Treasury yield rose dramatically. Generally, in a crisis like this, investors would flock to Treasury bonds (a flight to safety), which would drive down the yield—not up.

IRAs as One of the Emergency Fund Sources

If you ask whether you can borrow from an IRA (Individual Retirement Account), you would generally get a resounding “No.” However, there are several ways to take money out for short-term emergency purposes. This article explores some of those options.

Before we go on, we want to advise that borrowing or withdrawing money from retirement savings accounts is generally a bad idea and should be treated as a last-resort option. The reason is that your retirement savings are meant for your retirement, and messing with them could (seriously) affect your retirement future.

60-Day Rollover Provision

You can withdraw funds from your IRA and redeposit the same amount into the same or another IRA within 60 days. This effectively acts as a short-term, interest-free loan. However, this can only be done once every 12 months across all your IRAs. Failing to redeposit within 60 days results in the withdrawal being treated as a taxable distribution, and if you’re under 59½, it may also incur a 10% early withdrawal penalty.

Emergency Withdrawals under SECURE 2.0

Under the SECURE 2.0 Act, you can withdraw up to $1,000 annually from your IRA for emergency expenses without the 10% early withdrawal penalty. You have three years to repay the amount to avoid income taxes on the distribution. However, you cannot make another emergency withdrawal within that period unless the previous amount is repaid.

Penalty-Free Withdrawals for Specific Situations

Certain circumstances allow for penalty-free early withdrawals from an IRA, though income taxes may still apply:

- First-time home purchase (up to $10,000)

- Qualified education expenses

- Unreimbursed medical expenses exceeding 7.5% of your adjusted gross income

- Permanent disability

- Health insurance premiums while unemployed

- Qualified birth or adoption expenses (up to $5,000)

- Certain disaster-related expenses (up to $22,000)

Roth IRA Contributions

If you have a Roth IRA, you can withdraw your contributions (but not earnings) at any time without taxes or penalties, provided the account has been open for at least five years.

Other Options

Before tapping into your IRA, consider other emergency funding sources:

- Personal loans

- 0% introductory APR credit cards

- Home equity loans or lines of credit

- Borrowing from a 401(k) plan, if available — see Need to Withdraw From Your 401(k)? Follow This Order: Hardship Withdrawal, 401(k) Loan, and Penalty Withdrawal

For more information, refer to How to Borrow From an IRA?

Tools & Tips: The Gotcha in Maximum Solo 401(k) or SEP IRA Contribution Limits

The most common mistake is misunderstanding that the employer contribution amount in Solo 401(k) contribution limit is up to 20% of adjusted net earnings, not 25% as stated in the usual IRS instructions. This is because, in the IRS instructions, adjusted net earnings must first subtract the employer contribution before applying the 25%. When solved algebraically, this results in a 20% effective rate instead of 25%.

Let’s explain this in more details:

Per IRS instructions, employer contributions are always made on a pre-tax basis, reducing your taxable income. The above 25% of your compensation technically is after your employer contribution! So this is a circular dependency. In the following, we show the 25% should be actually 20% of your earned income, NOT the commonly mistaken 25%!

- Assume X is the employer contribution and E is your earned income, based on the IRS instruction, to maximize X, we have

- X=25%*(E-X) as E-X is your compensation

- Solved the above, we get X=20%*E!

We have updated our Solo 401(k) Maximum Contribution Calculator.

The above is also applicable to SEP IRA! In a word, it should be 20% of your adjusted net earnings, not 25%!

Please refer to Solo 401(k) Annual Contribution Limits: Employee and Employer Contributions for more details.

Market Overview

With the back-and-forth tariff policy changes—and finally the 90-day reciprocal tax deferral along with electronics exemptions—stocks have recovered a bit. However, we want to point out that U.S. stocks are still clearly in a downtrend.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 6.8% | -4.7% | -7.1% | -7.2% | 8.1% | -0.8% |

| Foreign Stocks | 7.9% | -5.6% | 4.6% | -5.6% | 4.7% | 1.2% |

| US REITs | 4.2% | -6.8% | -1.4% | -10.4% | 8.4% | -1.2% |

| Emerging Market Stocks | 5.5% | -6.7% | 2.0% | -9.8% | 4.9% | -0.8% |

| Bonds | -0.8% | -0.7% | 1.8% | -1.1% | 4.8% | 0.8% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Staying the course!

Struggle to Find Your Old Retirement Accounts?

Find Tools and Calculators That Provide Quick Help