Maximize Your Cash Returns

In this issue:

- Latest in Retirement Savings & Personal Finance: Inflation Pressure and 401(k) as Rainy-Day Fund

- Maximize Your Cash Returns

- Good Funds: Capital Group ETFs

- Market Overview

Latest in Retirement Savings & Personal Finance: Inflation Pressure and 401(k) as Rainy-Day Fund

Inflation continues to pressure low- and middle-income Americans

Inflation remains a top financial concern for Americans, with many feeling that their income isn’t keeping pace. This sentiment is echoed in reports highlighting that most Americans struggle to maintain their previous standard of living, leading to reduced discretionary spending and increased reliance on credit. This is especially true if ongoing tariff rates are raised on many imported products and goods, forcing companies to increase prices to offset the tariffs. Naturally, rising prices will directly impact the daily lives of low- and middle-income Americans.

401(k) Accounts as Emergency Funds

There’s a growing trend of individuals tapping into their 401(k) retirement accounts to address immediate financial needs. In 2024, a record 4.8% of account holders made early withdrawals, up from 3.6% in 2023. This shift underscores the financial pressures many face, prompting them to use long-term savings for short-term emergencies. We strongly advocate against tapping into retirement accounts if possible.

Leveraging Tax Refunds for Retirement Savings

With tax season underway, we recommend channeling tax refunds into retirement accounts. Options like traditional IRAs, Roth IRAs, 401(k)s, and Health Savings Accounts (HSAs) offer tax advantages and can significantly bolster retirement savings over time.

Maximize Your Cash Returns

Many people simply use their bank checking and savings accounts for cash. However, these accounts are still paying almost nothing in interest. For example, as of the last check, Bank of America offers just 0.02% interest on their checking and savings accounts—an absurdly low rate. Yet, many consumers continue to accept this without seeking better alternatives.

But there are better alternatives. One option is to invest in money market funds through your investment brokerage. Major brokerages like Fidelity, Schwab, and Vanguard now offer money market funds that pay significantly higher interest rates compared to traditional bank accounts.

Before we explore these options, let’s first understand the different types of savings vehicles available:

What are money market funds?

A money market fund is a type of mutual fund that invests in low-risk, short-term debt securities such as government bonds, certificates of deposit, and commercial paper. The primary goal of a money market fund is to provide investors with a relatively safe place to park their cash while earning a slightly higher return than traditional savings accounts or other cash investments. These funds are typically managed to maintain a stable net asset value (NAV) of $1 per share, making them a popular choice for investors looking to preserve capital and earn some income with minimal risk.

A money market fund’s NAV is allowed to fluctuate within a narrow range of 0.5% above or below the stable $1.00 per share value. This means the NAV may be reported as $1.005 or $0.995 per share without requiring corrective action. However, if the NAV falls outside this range, the fund must take steps to restore stability. These measures may include waiving fees, suspending redemptions, or liquidating assets to maintain the fund’s value.

Other regulations require that money market funds invest in ultra-short-term debt securities and high-quality debt instruments. For more detailed information, please refer to this article.

To summarize, a money market fund must:

- Maintain its NAV within a narrow range of 0.5% above or below the stable $1.00 per share value.

- It needs to hold enough short-term debt securities, with 30% having a 7-day maturity and 60% having a 60-day maturity, to manage interest rate risk effectively.

- It needs to hold high-quality debt securities to mitigate credit risk.

- Take corrective measures if the NAV falls below the established threshold, such as waiving fees or liquidating assets.

Types of Money Market Options

There are three types of money market options:

- Treasury Money Market Funds: These funds are considered as safe as FDIC-insured bank accounts because they invest in short-term government debt, such as T-bills. Since these government securities are fully backed by the U.S. government, they carry a similar safety profile to FDIC-insured accounts. It’s important to note that when you purchase shares in such a fund, you are essentially holding the underlying government debts collectively with other shareholders.

- Prime Money Market Funds: These funds include a mix of corporate debt, which allows for slightly higher returns compared to Treasury money market funds. However, this increase in potential returns comes with more risk, as corporate debt can be subject to credit risk and other market fluctuations.

- Bank Money Market Accounts: These accounts offer FDIC protection, providing security for your deposits. However, they often come with lower interest rates compared to money market funds, which may limit the potential returns on your investment.

Money market auto sweep and cash movement

Many brokerage firms offer features that allow investors to access their funds similarly to cash. Here’s how ACH transfers and debit cards facilitate this:

ACH Transfers:

The Automated Clearing House (ACH) network enables electronic fund transfers between financial institutions in the United States. Investors can utilize ACH transfers to move money between their money market mutual funds and external bank accounts.

Debit Cards:

Certain brokerage firms issue debit cards linked to investors’ money market funds, enabling:

- Purchases: Investors can make purchases at retailers or online platforms directly from their money market funds.

- ATM Withdrawals: Access to cash through ATMs is facilitated, allowing for immediate liquidity.

Fidelity and Schwab both offer debit cards linked to their brokerage accounts. Fidelity even provides an auto-sweep feature for uninvested cash into its Government Money Market Fund (SPAXX), effectively allowing you to treat your SPAXX investment as cash. Unfortunately, Schwab does not offer this auto-sweep feature, meaning you’ll need to buy and sell money market funds manually. However, Schwab’s debit cards are linked to your brokerage accounts, allowing you to spend the cash in your brokerage account using the debit card.

What are the money market funds paying these days?

Most popular money market funds

| Symbol | Fund Name | 7-Day Yield | Net Asset |

|---|---|---|---|

| SNAXX | Schwab Value Advantage Money Fund® Ultra Shares | 4.3351 | 121.192 B |

| VMFXX | Vanguard Federal Money Market Fund Investor Shares | 4.2572 | 334.587 B |

| SWVXX | Schwab Value Advantage Money Fund® Investor Shares | 4.1851 | 220.634 B |

| SNOXX | Schwab Treasury Obligations Money Fund™ – Investor Shares | 4.0888 | 36.455 B |

| SNVXX | Schwab Government Money Fund™ – Investor Shares | 4.0883 | 28.763 B |

| SPRXX | Fidelity Money Market Fund | 4.04 | 12.201 B |

| SNSXX | Schwab U.S. Treasury Money Fund™ Investor Shares | 4.0171 | 36.088 B |

| SPAXX | Fidelity Government Money Market Fund | 4 | 354.027 B |

The MyPlanIQ Money Fund Market Center page has comprehensive lists of money market mutual funds and money market ETFs.

In summary, there are several alternatives available. You can also find online savings accounts that offer higher interest rates, but many of these rates are promotional and designed to attract new customers. Once the promotional period ends, the rates typically drop back down to more standard levels.

Good Funds: Capital Group ETFs

Many people are familiar with American Funds in their 401(k) retirement plans. Often, you’ll see funds like AGTHX (Capital Group GROWTH FUND OF AMERICA CLASS A) or CWGIX (CAPITAL WORLD GROWTH & INCOME FUND CLASS A). A common question we hear is what options are available for IRA investments, which offer a much wider range of choices, including No-Load, No-Transaction-Fee mutual funds (we strongly advise against using load or transaction-fee mutual funds). Additionally, you can invest in virtually all ETFs available in the market, including those from Capital Group.

Here are some Capital Group ETFs you may consider for your IRA portfolio:

| Asset Class | YTD | 1Yr AR | 3Yr AR |

|---|---|---|---|

| CGUS (Capital Group Core Equity ETF) | -3.86% | 11.11% | 12.37% |

| CGDV (Capital Group Dividend Value ETF) | 1.64% | 15.35% | 14.87% |

| CGDG (Capital Group Dividend Growers ETF) | 3.95% | 10.87% | NA |

| CGGR (Capital Group Growth ETF) | -8.34% | 9.46% | 12.60% |

| CGIC (Capital Group International Core Equity ETF) | 8.52% | NA | NA |

| CGCP (Capital Group Core Plus Income ETF) | 1.53% | 3.90% | 0.44% |

The above funds are all solid core options for building a long-term portfolio.

Market Overview

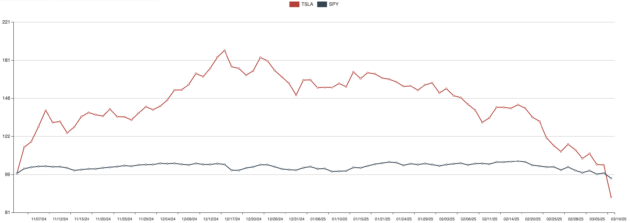

Well, it didn’t take long. The Trump administration signaled that it might not support asset markets. Spooked by a string of negative news—including tariffs, declining consumer confidence, and still-elevated stock valuations—investors abandoned stocks in droves, driving prices down sharply. As of this writing, for example, Tesla (TSLA), one of the meme stocks that initially seemed to benefit from the new administration, is now down more than 50% from its peak, even falling below pre-election levels.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -4.0% | -7.3% | -7.0% | 3.2% | 11.0% | -0.8% |

| Foreign Stocks | 0.5% | 1.0% | -0.3% | 1.5% | 5.9% | 1.7% |

| US REITs | -3.0% | -0.1% | -4.6% | -3.9% | 7.7% | -0.8% |

| Emerging Market Stocks | 1.4% | -0.9% | -5.2% | 2.3% | 7.7% | 1.1% |

| Bonds | -0.4% | 1.4% | -0.2% | -1.6% | 3.4% | 0.5% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Of course, during times like this, we want to remind our readers that retirement savings and investments are for the long term. You shouldn’t be swayed by short-term market volatility as long as you have a solid asset allocation strategy. If you’re not familiar with these concepts, now is a great time to learn and gain a better understanding. For those who have already chosen a strong investment path—stay the course.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?