One Fund Does It All

In this issue:

- Latest in Retirement Savings & Personal Finance: US Food & Engergy Inflation Charts, Empty Shelfs Coming? Part-time Contractors Rejoin on 401(k) Eligibility

- One Fund Does It All: Savings & Investing in 401(k) Might Not Be That Intimidating

- Tools & Tips: Retirement Spending Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: US Food & Engergy Inflation Charts, Empty Shelfs Coming? Part-time Contractors Rejoin on 401(k) Eligibility

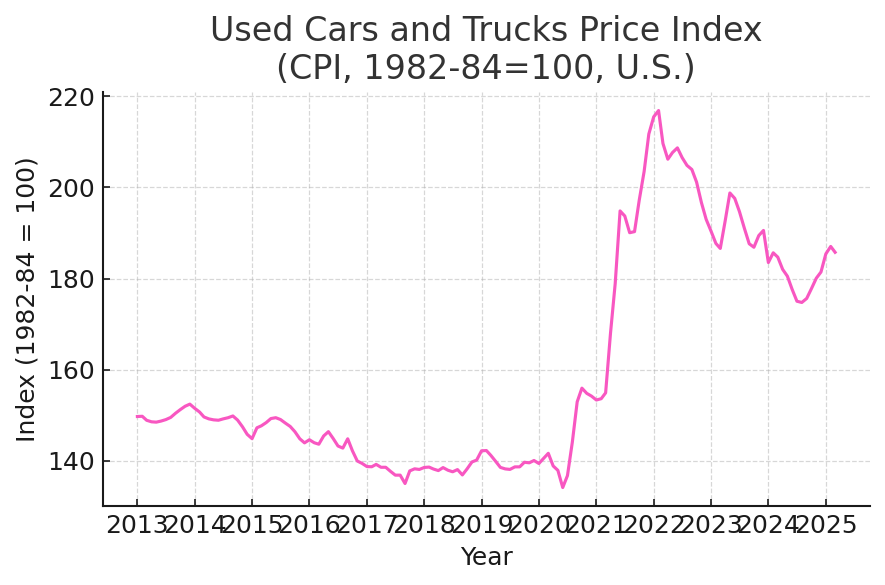

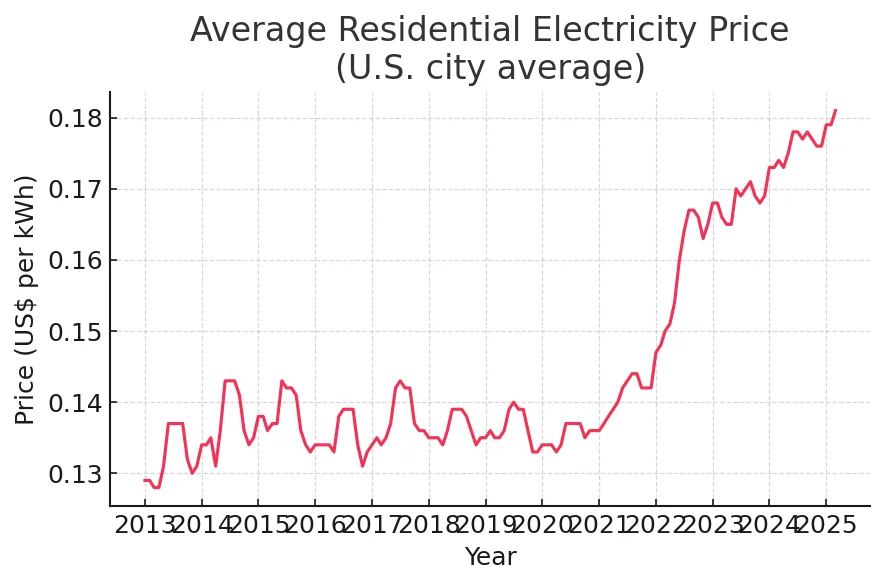

US Food & Energy Price Charts

Presenting the following four charts:

Gas prices are now at 2013 levels, not much inflation. Frankly, other than eggs, used cars and electricity aren’t doing that bad either. The problem is that we have been through a long low-inflation decade, and thus everything now seems to be rising!

Empty Shelfs Coming?

Lately you might have seen the headlines — warnings about empty store shelves. Multiple reports said that CEOs from some of the biggest retail chains sat down with President Trump and told him straight: if the trade war drags on too long, it’s going to mean real shortages. From what we’re seeing in different reports, it looks like U.S. consumers will probably start feeling the hit from the new tariffs around mid to late May 2025. There’s usually a bit of a lag — about six to eight weeks — between when tariffs kick in and when you actually see it on the price tags. Makes sense if you think about it… it takes time for stuff to get made, shipped across the ocean, stocked on the shelves.

So brace for the impact.

Part-time Workers Rejoin on 401(k) Eligibility

To try and boost retirement savings for more workers — especially part-timers — both SECURE 2.0 and the earlier 2019 SECURE 1.0 laws made it easier to qualify. Before, an employer could make you work up to 1,000 hours in a year before you were even allowed into a 401(k) or 403(b) plan. But under SECURE 2.0, starting with plan years after December 31, 2024, the rules got loosened. If you put in at least 500 hours two years in a row, you’re in — they call it “long-term part-time employees.” So if you hit 500 hours in both 2023 and 2024, you officially became eligible January 1, 2025.

By the way, if you do not meet the above requirements, there’s no harm to ask whether the company can be generous to offer 401(k) plan savings to you: a company can always choose to be more generous if it wants. They don’t have to wait for a part-time employee to hit the 500-hours-in-two-years minimum. The SECURE Act and SECURE 2.0 just lay out the floor, but employers are free to set easier, more open rules. Some might even let every employee, no matter how many hours they work, jump into the 401(k) plan right from the start. And if a company goes that route — no service requirements, no hours thresholds — then all that LTPT (long-term part-time) rule stuff basically doesn’t apply at all. Something to keep in mind!

One Fund Does It All: Savings & Investing in 401(k) Might Not Be That Intimidating

When you’re just starting out with a 401(k) or any retirement plan, the number of choices can feel almost paralyzing. So many funds, so many opinions — it’s easy to get overwhelmed and end up doing nothing. That’s why the idea of a simple one-fund portfolio has caught on. Whether through a target date fund or a balanced 60/40 fund, the basic goal is the same: give you a solid, diversified, low-maintenance way to invest without needing to constantly second-guess yourself.

These days, most 401(k) plans already offer target date funds. They often even pick one for you automatically as the default investment. So for many people, the easiest and most effective option might already be working in the background without them even realizing it. And even if you’re a little more experienced, honestly, a good target date fund or balanced fund can still get the job done. In fact they probably are doing as well or even better than most participants who are just picking funds randomly without any real system behind it.

Target date funds are the easiest starting point for most people — just pick the year closest to when you expect to retire, and the fund adjusts stocks and bonds exposure over time for you. If target funds aren’t available, a balanced fund like VSMGX (VANGUARD LIFESTRATEGY MODERATE GROWTH FUND INVESTOR SHARES) or AOR (iShares Core Growth Allocation ETF) can offer a good choice too. Of course, most time, you’ll look at whether your plan offers a balanced fund. We prefer a low cost index based balance fund like VSGMX. Just check out its expense cost before committing to it.

If you want to dig deeper into why a simple one-fund approach can be so powerful (and see some real-life examples), you can check out the full article here: The One-Fund 401(k) Portfolio: Simple Yet Does Its Job.

Let’s also see how well they do for retirement spending in the next section.

Tools & Tips: Retirement Spending Calculator

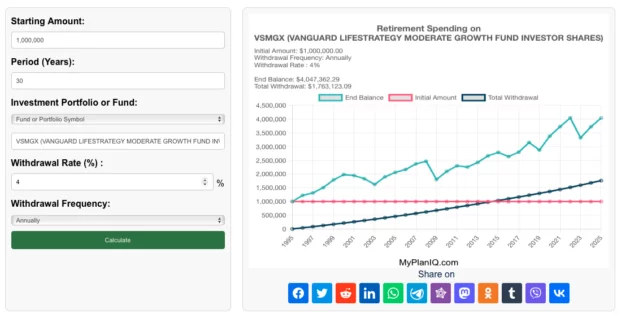

MyPlanIQ’s Retirement Spending Calculator Based on a Portfolio, Fund, or Stock helps you estimate how long your retirement savings will could have lasted based on historical investment returns. By entering your starting amount, the time period, withdrawal rate, and choosing an investment option (such as a portfolio, fund, or stock), the calculator generates a detailed chart showing end balance and total withdrawals in the time period given.

In the example below, we enter VSMGX into the “Investment Portfolio or Fund” input and set the “Period (Years)” to 30. That basically means we’re looking at the past 30 years of history: starting from 1995 to see how the fund would have performed if you had made annual withdrawals at a 4% rate.

You can see that your wealth (completely in this one fund) has actually grown from $1 million to $4 million, even after taking 4% (inflation-adjusted) out every year for spending!

However, if you were retired in 2000, things become worse: you actually have only $800k left after spending a total of $1.36 million.

So indeed, watch out when you are retiring at a market peak like 2000. Actually, today’s markets are very similar to that in 2000 — extremely high stock valuation and much excitement and speculation on AIs and cryptos!

Of course, if you adopt MyPlanIQ’s simple tactical portfolio that invests in S&P 500 tactically by trying to switch to bonds or cash when it determines a market downturn — such as this portfolio P_73817 (P Composite Momentum Market VFINX) — you would have done much better: you would again accumulate $4 million by now even after withdrawing annually 4% for the past 25 years.

See What MyPlan Premium Subscripton Offer Here.

Market Overview

US stocks rose last week as investors were hopeful that the tariff situation with major trading blocs, especially with China, would soon be deescalated. As of right now, however, not very much actual progress has been made. As we stated before, if this keeps dragging on, the US economy (as well as other economies in the world) will see material damage.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 4.6% | -0.9% | -9.2% | -4.3% | 9.7% | 0.0% |

| Foreign Stocks | 3.4% | 1.2% | 3.7% | 1.5% | 8.1% | 3.6% |

| US REITs | 0.2% | -3.1% | -4.1% | -9.2% | 10.7% | -1.1% |

| Emerging Market Stocks | 3.3% | -1.1% | 0.6% | -4.7% | 6.3% | 0.9% |

| Bonds | 0.6% | -0.1% | 1.6% | 0.6% | 5.9% | 1.7% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Staying the course!

Struggle to Find Your Old Retirement Accounts?

Find Tools and Calculators That Provide Quick Help