Outsaving Regular Workers: How Gig Workers & Entrepreneurs Can Save 3x More for Retirement—Up to $70K Tax-Deferred!

In this issue:

- Latest in Retirement Savings & Personal Finance

- Outsaving Regular Workers: How Gig Workers & Entrepreneurs Can Save 3x More for Retirement—Up to $70K Tax-Deferred!

- Solo 401(k) Maximum Contribution Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance

Here is some of the latest news:

401(k) Participation Rates Up But Still Not Enough

Per The Wall Street Journal, for the first time, half of private-sector workers in the U.S. are participating in 401(k) plans, compared to only 43% a decade ago. Here are some numbers:

- 85% of private industry workers lack access to a defined benefit pension plan, so they must rely on self-funded 401(k) plans for retirement.

- 70% of private-sector workers have access to 401(k) savings plans, meaning 30% do not. Subtracting the 15% who have access to a pension plan, that leaves 15% with neither a 401(k) nor a pension plan.

- Among those with 401(k) access, 20% are still not contributing. Adding this to the 15% without access to either a 401(k) or a pension, a total of 35% of private-sector workers are not saving anything for retirement and have no pension.

So, 35% of private-sector workers will have to rely entirely on Social Security and government assistance in retirement—not what you’d expect from a wealthy nation like the U.S!

Working Longer While Life Expectancy Declines

Americans also experience:

Increasing Retirement Age:

- In 1991, the average retirement age among Americans was 57 years.

- As of 2024, this average has risen to 62 years, representing an increase of about 8.8%. 23% of workers expected to retire at age 70 or older or not at all!

Declining Life Expectancy:

- In 2014, the average life expectancy in the U.S. peaked at 78.8 years.

- By 2021, this figure had decreased to 76.1 years, marking a decline of approximately 3.4%.

- By 2023, it recovered back to 78.4 years, almost to the pre-pandemic level.

- However, the U.S. still lags behind other affluent nations. In 2023, the average life expectancy in comparable countries was 82.5 years, giving them a 4.1-year advantage over the U.S.

Reevaluating Retirement Withdrawal Rates

Instead of the popular 4% withdrawal rate, Morningstar suggests in a new research report that retirees searching for a safe starting withdrawal rate should go no higher than 3.7%. That gives them a 90% probability of having some money remaining at the end of a 30-year retirement period. This recommendation considers current high equity valuations and lower fixed-income yields, emphasizing the need for flexible spending strategies and delayed Social Security claims to maximize benefits.

In general, it makes sense to reduce your withdrawal rate (or expected spending amount) when markets are high, as they will inevitably experience a downturn and take time to recover. Put simply, the higher the current stock and bond markets are, the lower future returns will be. So, prepare ahead.

Outsaving Regular Workers: How Gig Workers & Entrepreneurs Can Save 3x More for Retirement—Up to $70K Tax-Deferred!

Most gig workers, freelancers, and entrepreneurs don’t realize they can stash away far more for retirement than traditional full-time employees. This group of people includes, but is not limited to:

- Gig workers like Uber Drivers, Door Dash delivery people and many others

- Freelancers like independent software developers, high tech part-time consultants, part-time accountants etc.

- Entrepreneurs like small business owners and many physicians.

For these workers, opening a SEP IRA or Solo 401(k) retirement savings account at brokerages like Fidelity, Schwab, or Vanguard is straightforward. Most of these brokerages don’t charge any fees these days. With a Solo 401(k), if your plan’s assets total less than $250,000, you won’t need to file additional IRS documents, making it as simple as opening an IRA.

In 2025, a Solo 401(k) allows total contributions of up to $70,000, combining both employee and employer contributions. Since you’re both the employee and the employer in self-employment, you can take full advantage of this higher limit. A SEP IRA also lets self-employed individuals contribute as the “employer,” though it doesn’t allow separate employee deferrals.

By contrast, a traditional 401(k) limits employee deferrals to just $23,500. That’s a massive gap—one that lets gig workers and small business owners slash taxable income and save far more for retirement than regular employees.

And here’s the kicker—these plans aren’t just for full-time entrepreneurs. If you have a side gig on top of a regular job, you can still open a Solo 401(k) and contribute as both an employee and employer, maximizing savings across multiple income streams.

Bottom line? Gig workers, freelancers, and self-employed professionals have access to far greater tax-deferred benefits than regular employees—$70K vs. $23.5K. Most people have no idea they could be saving this much more!

Read more articles and access to calculators on Retirement Plans for Self-Employed Workers and Small Business Owners page.

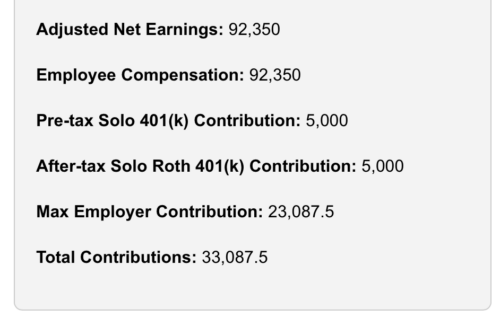

Tools & Tips: Solo 401(k) Maximum Contribution Calculator

The Solo 401(k) Maximum Contribution Calculator helps self-employed individuals and small business owners determine their maximum contributions to a Solo 401(k) plan, including Roth contributions and employer contributions. In the following example, the calculator shows you can save up to $33K if you earn $100K a year.

You enter the inputs:

Once you press ‘Calculate’, the output will be:

Important note:

- Employer Contribution Adjustment: The employer contribution cannot exceed:

- 25% of Adjusted Net Earnings:

- The amount left after employee contributions, or

- The IRS-defined maximum total contribution limit.

- 25% of Adjusted Net Earnings:

Market Overview

A few developments last week on the financial and economic fronts:

- The January jobs report showed a gain of 143,000 jobs, falling short of expectations but accompanied by upward revisions for prior months and a drop in the unemployment rate to 4.0%.

- The ISM Manufacturing PMI indicated expansion in January for the first time in over two years, signaling a recovery in the manufacturing sector.

- Bonds gained as yields declined amid weaker-than-expected employment data.

- Corporate earnings reports were mostly positive, with 77% of S&P 500 companies surpassing expectations and reporting an average earnings growth of 16.4%.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | 1.5% | 2.0% | 4.5% | 10.7% | 23.6% | 8.5% |

| Foreign Stocks | 2.2% | 5.4% | 4.1% | 1.7% | 9.8% | 4.7% |

| US REITs | 0.0% | 2.1% | -2.3% | 1.1% | 11.6% | 2.5% |

| Emerging Market Stocks | 1.5% | 4.1% | 1.0% | 2.2% | 11.8% | 4.1% |

| Bonds | 0.2% | 0.8% | 0.4% | -1.1% | 3.7% | 0.8% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?