Introduction

When you just start working, retirement usually feels like something too far away to think about seriously. Maybe even silly to worry about. But, in reality, this is probably one of the biggest advantages you can give yourself if you want real wealth down the road. For many new workers, the first real investment experience comes through some kind of employer plan like a 401(k), or a 403(b) if you’re in nonprofit or government. And inside most of these plans these days, Target Date Funds (TDFs) are getting more and more popular. These are the reasonable chocies for people who just start out.

Understanding Retirement Accounts

Most U.S. workers have access to retirement savings through employer-sponsored accounts such as:

- 401(k): Offered by private-sector employers, often with matching contributions.

- 403(b): Similar to 401(k), but offered by public schools, nonprofits, and certain hospitals.

- 457(b): Used mainly by government employees.

- IRAs (Traditional and Roth): Individual Retirement Accounts available outside employer plans.

One thing all these plans have tax advantage. Whether you’re putting in money pre-tax (the traditional way) or after-tax (Roth style), the real magic is that your investments get to grow without the usual annual tax bite, at least for a long while. It might seem to be small, but over years and decades, it makes a huge difference.

Default Investment Options in 401(k) Plans

Nowadays, most 401(k) plans just sign you up automatically to some default investment option. Usually, that’s a Target Date Fund tied to when you’re “supposed” to retire. So if you’re, say, 25 years old, you might find yourself in a 2060 or even 2065 fund without ever picking it yourself. The idea behind these defaults is simple enough: help people get started with a diversified portfolio without forcing them to make a hundred complicated choices right out of the gate.

What Are Target Date Funds?

A Target Date Fund is basically a mutual fund or an ETF that shifts stocks and bonds exposure over time. If you think you’ll retire around 2060, you pick a 2060 fund. In the early years, it’s heavy on growth (usually around 90% in stocks), because you’ve got time to ride out the storms. Then, slowly, it starts dialing back the risk, adding more bonds and safer stuff as you get closer to needing the money.

Why Target Date Funds Are Ideal for Young Professionals

- Simplicity: You pick one fund aligned with your retirement year, and the fund handles everything else.

- Diversification: Each fund is a portfolio of many stocks and bonds.

- Automatic Rebalancing: Adjusts the asset mix over time without manual intervention.

- Low Maintenance: No need to pick multiple funds or worry about market timing.

This kind of “single-fund” approach actually lines up pretty well with the thinking of groups like the Bogleheads who believe in low-cost, broadly diversified investing without a lot of messing around. A lot of Bogleheads, and even plenty of financial advisors, would tell you that one good target date fund is enough for most people. Trying to mix a bunch of funds together sounds smart, but more often it just adds hidden risks or messy overlaps, especially if you’re still pretty new to all this.

Top Target Date 2060 Funds Compared

These are among the most popular Target Date Fund series in the U.S., so chances are you’ve seen one of them in your retirement plan menu.

| Provider | Fund Name | Ticker | Stocks (%) | Bonds (%) | Expense Ratio | 1-Year Return | 5-Year Return |

|---|---|---|---|---|---|---|---|

| Vanguard | Target Retirement 2060 Inv | VTTSX | ~90% | ~10% | 0.08% | 13.3% | 11.3% |

| Fidelity (Freedom) | Freedom 2060 Inv | FDKVX | ~90% | ~10% | 0.75% | ~12.5% | ~11.0% |

| T. Rowe Price | Retirement 2060 Inv | TRRLX | ~95% | ~5% | 0.64% | ~13.0% | ~11.5% |

| BlackRock | LifePath Index 2060 K | LIZKX | ~95% | ~5% | 0.14% | 12.9% | 11.6% |

| American Funds | 2060 Target Date Retirement R6 | RFUTX | ~90% | ~10% | 0.39% | 12.9% | 11.6% |

| State Street | Target Retirement 2060 Index | SSDWX | ~95% | ~5% | ~0.10% | ~13.0% | ~11.5% |

| JP Morgan | SmartRetirement 2060 R6 | JTSHX | ~90% | ~10% | ~0.50% | ~13.0% | ~11.0% |

| TIAA/Nuveen | Lifecycle 2060 Inst | TLXNX | ~90% | ~10% | ~0.40% | ~13.0% | ~11.2% |

| Principal | Lifetime 2060 Inst | PLTRX | ~90% | ~10% | 0.44% | ~13.0% | ~11.0% |

| Schwab | Target 2060 Index | SWYNX | ~97% | ~3% | 0.08% | ~12.9% | ~11.0% |

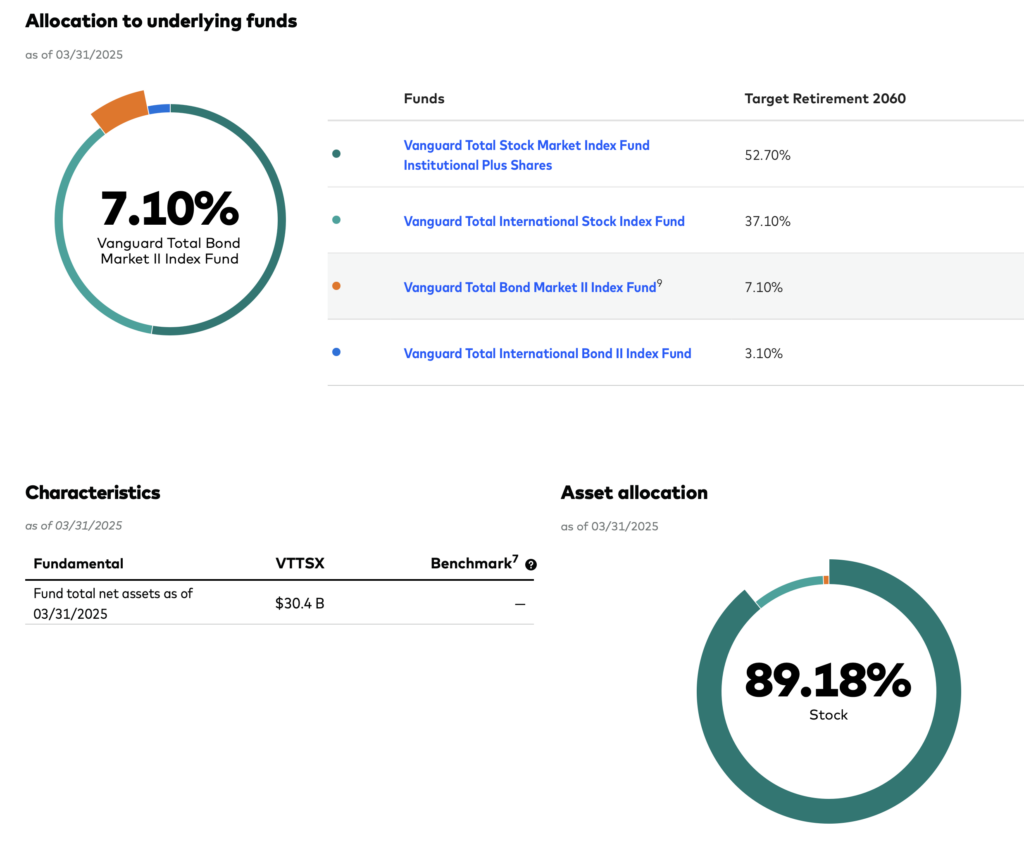

The following shows the allocation of Vanguard Target Date 2060 Fund.

Suppose you are to retire at age 65; a 2060 fund means you are currently 30 years old. 90% in stocks indicates a prevalent belief that for people at this young age, you can ride out stocks’ ups and downs for the next 35 years before you retire in 2060.

The following compares these funds’ total returns (as of 4/25/2025):

| Name | YTD Return | 1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR | Inception |

|---|---|---|---|---|---|---|

| VTTSX (VANGUARD TARGET RETIREMENT 2060 FUND INVESTOR SHARES) | NA | 23.57% | 4.75% | 9.26% | 8.37% | 10.05% |

| FDKVX (FIDELITY FREEDOM 2060 FUND FIDELITY FREEDOM 2060 FUND) | NA | 23.66% | 1.25% | 6.09% | 6.84% | 8.01% |

| TRRLX (T. ROWE PRICE RETIREMENT 2060 FUND T. ROWE PRICE RETIREMENT 2060 FUND) | NA | 22.32% | 2.12% | 7.99% | 8.14% | 9.44% |

| LIZKX (BlackRock LifePath Index 2060 Fund Class) | NA | 26.20% | 6.91% | 10.81% | NA | 11.12% |

| RFUTX (AMERICAN FUNDS 2060 TARGET DATE RETIREMENT FUND CLASS R-6) | NA | 23.65% | 2.51% | 8.22% | NA | 9.78% |

| TLXNX (TIAA-CREF LIFECYCLE 2060 FUND INSTITUTIONAL CLASS) | NA | 23.43% | 2.70% | 7.93% | 8.32% | 9.51% |

| PLTRX (PRINCIPAL LIFETIME 2060 FUND R-1) | NA | 18.69% | 0.08% | 5.80% | 6.17% | 7.66% |

| SWYNX (SCHWAB TARGET 2060 INDEX FUND INSTITUTIONAL SHARES) | NA | 25.79% | 6.63% | 10.57% | NA | 11.06% |

| SSDWX (STATE STREET TARGET RETIREMENT 2060 FUND CLASS I) | NA | 23.14% | 2.72% | 8.06% | 7.79% | 9.32% |

Note: Inception is 8/26/2016 for comparison purpose.

Active vs. Index: Differences Within the Same Category

Even though all Target Date Funds kind of move along the same path — heavy on stocks early, then easing off as you get close to retirement — they’re not all built the same way. Some, like the ones from Vanguard, Schwab, State Street, BlackRock, stick to index investing. Meaning, they just try to match the market, keep costs low, stay out of the way. Others, like Fidelity Freedom or T. Rowe Price and American Funds, are more active — trying to beat the market by shifting around allocations or picking individual securities. Of course, with active management usually comes higher fees… and more unpredictability in the returns. So even if you’re just using one fund, it’s still worth knowing what’s actually under the hood. You can certainly get some idea from the above table.

Conclusions

For young professionals just starting out, Target Date Funds offer something pretty powerful, as they roll a mix of simplicity, diversification, and long-term growth into one. Pick a low-cost one, stick with it, and you’ve got a good shot at building wealth steadily over your whole career without needing to constantly tinker or guess what’s next. They can certainly serve as a good starting point, or even just a more permanent solution.