Lazy portfolios, which consist of low-cost index funds or exchange-traded funds (ETFs), are designed to provide diversified, hands-off investment strategies that perform well across various market conditions. However, not all lazy portfolios behave the same way during bull markets, bear markets, or periods of volatility. Understanding how these portfolios perform under different circumstances and concepts like maximum drawdown , rolling returns , and asset allocatio can help you navigate through various market cycles.

Background: Key Concepts and Portfolio Categories

Before diving into performance metrics, let’s establish some foundational knowledge:

Maximum Drawdown

Maximum drawdown measures the largest decline from peak to trough in a portfolio’s value during a specific period. For example, if your portfolio drops from 100,000 to 80,000 before recovering, the maximum drawdown is 20%. This metric helps investors understand potential losses during market downturns and assess their risk tolerance.

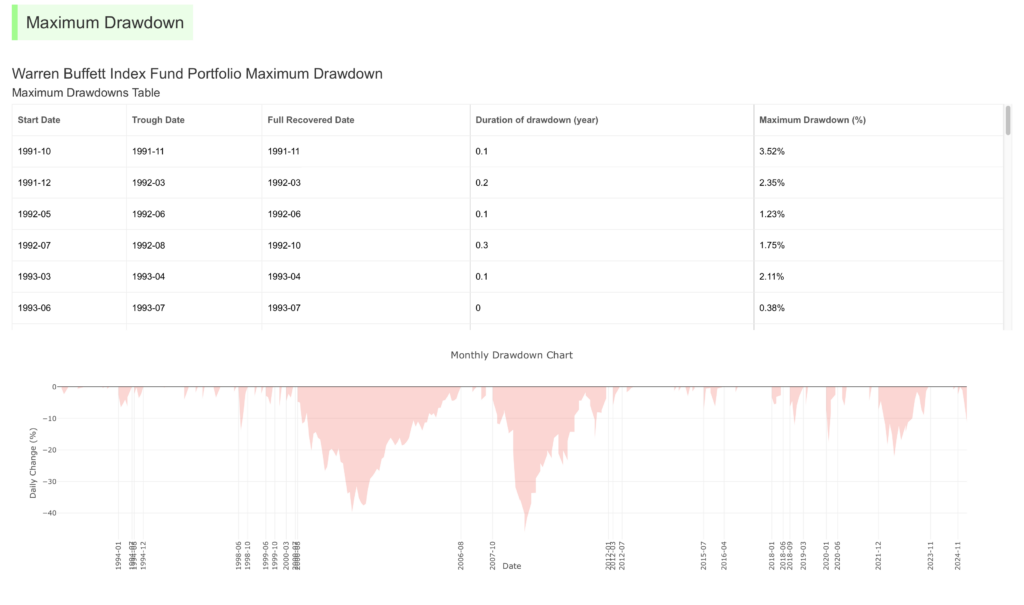

In MyPlanIQ, every portfolio has its maximum drawdown data. For example, we maintain the following table and chart for the maximum drawdowns for Warren Buffett Index Fund Portfolio:

Rolling Returns

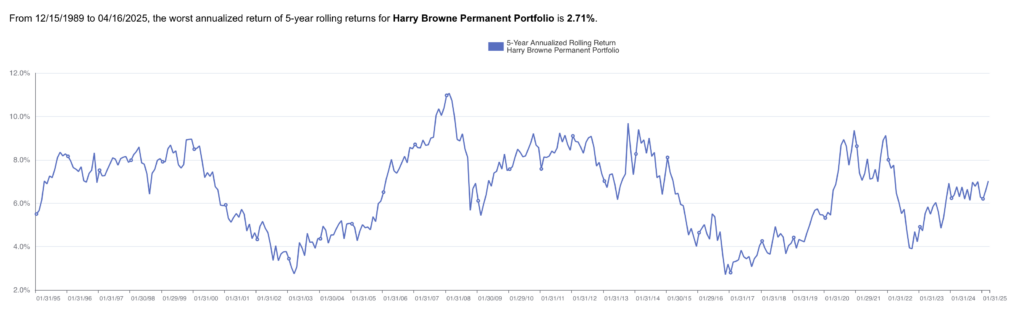

Rolling returns analyze performance over overlapping periods, such as every possible 3-year or 10-year window within a given timeframe. These rolling return serieses or charts illustrate how well a portfolio behaves in any particular period such as 3-year periods. For example, the following chart shows the rolling 5-year return chart for Harry Browne Permanent Portfolio:

From the above chart, we can see that since 1995, if you invest in any time, you will get minimum 2.71% annualized return after 5 years. This would give you a sense of how smooth the portfolio is if you invest for a 5 year period.

Two Categories of Lazy Portfolios

Lazy portfolios generally fall into two categories:

- Traditional Lazy Portfolios: These focus on broad market exposure through U.S. stocks, international stocks, and bonds. They prioritize growth and are ideal for younger investors with longer time horizons.

- Non-Traditional Lazy Portfolios: These incorporate alternative assets like gold, cash, real estate, or inflation-protected bonds (TIPS). They emphasize stability and downside protection, making them suitable for risk-averse or near-retirement investors.

With this background in mind, let’s explore how traditional and non-traditional lazy portfolios perform in different market conditions.

Traditional Lazy Portfolios: Built for Growth

The most popular lazy portfolio is the Bogleheads Three Fund Portfolio, which provides a simple yet effective blend of domestic and international equities alongside fixed income. A typical allocation might look like this:

- VTI (Vanguard Total Stock Market ETF, 50%)

- VEA (Vanguard FTSE Developed Markets ETF, 30%)

- BND (Vanguard Total Bond Market ETF, 20%)

This structure balances domestic growth with global diversification and bond stability, making it a solid choice for long-term investors.

Performance in Bull Markets

During extended bull markets, traditional lazy portfolios tend to shine. For example, during the 2010–2021 bull market:

- The Bogleheads Three Fund Portfolio delivered an average compound annual growth rate (CAGR) of 10.2% .

- Volatility, measured by standard deviation, was relatively moderate at 13.8% .

- Maximum drawdown during the short correction in the Covid-19 pandemic reached about -17.4% , but these declines were quickly recovered due to strong equity performance.

In essence, traditional portfolios capture most of the upside in rising markets while relying on bonds to cushion mild downturns.

Performance in Bear Markets

While traditional portfolios excel in bull markets, they can be vulnerable during sharp downturns. For instance:

- During the 2008 financial crisis, the Three-Fund Portfolio lost more than -42.7%! This is a very large drawdown that might make some investors nervous.

- In the 2020 COVID crash (Q1), the portfolio dropped approximately -14% .

These losses highlight the sensitivity of traditional portfolios to equity shocks, even with bond diversification.

Non-Traditional Lazy Portfolios: Built for Stability

Non-traditional lazy portfolios take a different approach by including assets that don’t correlate closely with stocks or bonds. A classic example is Harry Browne Permanent Portfolio, which allocates equally across four asset classes:

- Stocks: 25%

- Long-Term Bonds: 25%

- Gold: 25%

- Cash or Short-Term Bonds: 25%

This design aims to thrive in various economic environments: prosperity, inflation, deflation, and recession.

Performance in Bull Markets

While robust in volatile markets, non-traditional portfolios lag behind in roaring bull markets. During the same 2010–2021 period:

- Average return was closer to 6.9% CAGR.

- Standard deviation was much lower at 6.1%, reflecting reduced volatility.

- However, the heavy allocation to non-equity assets caused significant underperformance during equity-led rallies, as can be seen to compare with 10.2% CAGR of Bogleheads Three Fund Portfolio.

In other words, non-traditional portfolios trade higher returns for greater peace of mind and stability.

Performance in Bear Markets

Non-traditional portfolios truly shine during bear markets, offering substantial downside protection. For example:

- During the 2008 financial crisis, the Permanent Portfolio fell less than -13.6% .

- In the 2020 COVID crash (Q1), the portfolio declined only around -1.7% .

The inclusion of gold and cash significantly dampens drawdowns, providing a smoother ride during turbulent times.

Risk Metrics: Beyond Simple Returns

The following are the return comparison for the two portfolios: from 7/26/2007 to 4/16/2025

| Name | YTD Return | 1Yr AR | 3Yr AR | 5Yr AR | 10Yr AR | 15Yr AR | 20Yr AR | Inception |

|---|---|---|---|---|---|---|---|---|

| Bogleheads Three Fund Portfolio | -3.74% | 6.37% | 5.63% | 10.69% | 7.35% | 8.35% | NA | 6.81% |

| Harry Browne Permanent Portfolio | 4.74% | 14.07% | 6.73% | 5.96% | 6.16% | 6.43% | 6.92% | 6.81% |

Investors often focus on returns without considering the risks involved. Let’s compare hypothetical 10-year performance scenarios using placeholder metrics:

| Metric | Traditional 3-Fund | Non-Traditional (Permenant ) |

|---|---|---|

| CAGR | 10.2% | 6.9% |

| Standard Deviation | 9.6% | 4.3% |

| Max Drawdown | -42.7% | -13.6% |

| Sharpe Ratio | 0.34 | 0.71 |

| Worst Rolling 3-Year | -5.5% | -0.8% |

The non-traditional portfolio exhibits lower volatility and greater consistency, albeit with capped returns. Conversely, the traditional portfolio delivers superior performance during expansionary periods but suffers sharper setbacks.

Rolling Returns: The Consistency Test

Rolling returns offer valuable insight into long-term portfolio behavior. Traditional portfolios can experience wide variations in rolling 10-year returns, ranging from 4% to 9% , depending on market conditions. In contrast, non-traditional portfolios—especially those with gold or TIPS—tend to deliver more stable 10-year returns in the 4.5%–6% range , even during chaotic periods.

If maximizing upside is your priority, traditional portfolios are the clear winner. If preserving capital with decent growth is more important, non-traditional portfolios shine.

Conclusion: Which Lazy Portfolio Suits Your Needs?

Choosing the right lazy portfolio depends on your individual goals, risk tolerance, and investment horizon. Here’s a simplified breakdown:

| Investor Type | Portfolio Type | Why? |

|---|---|---|

| Young, growth-oriented | Traditional (VTI/VEA/BND) | Higher returns over decades |

| Nearing retirement | Blended or non-traditional | Lower drawdowns, more stability |

| Risk-averse or preservation-focused | Permanent Portfolio | Smooth ride, inflation hedging |

For those seeking balance, hybrid portfolios—such as adding 5–10% gold or real assets to a traditional mix—can offer a middle ground.

Ultimately, the best lazy portfolio is the one you can stick with through both booms and busts. Whether you’re investing in an IRA, taxable account, or 401(k), understanding how these strategies perform in different market conditions will help you build a resilient retirement plan tailored to your needs.