The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

In this issue:

- Latest in Retirement Savings & Personal Finance: Tariff Liberation Day, Beefing Up Emergency Savings, and Consumer Confidence at Its Lowest

- Paying Off Debt or Funding Retirement? How to Decide When Every Dollar Counts

- Paying off Debt or Investing Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: Tariff Liberation Day, Beefing Up Emergency Savings, and Consumer Confidence at Its Lowest

Trump’s Tariff Liberation Day

On April 2, 2025, the Trump Administration will start to implement a series of new “reciprocal” tariffs aimed at reducing the United States’ reliance on foreign goods.

Economists and industry leaders have expressed concern that these tariffs may lead to higher consumer prices, retaliatory measures from affected countries, and potential disruptions to global trade. Despite these warnings, President Trump asserts that the tariffs will encourage domestic manufacturing and create a more balanced economic playing field for U.S. exports.

As “Liberation Day” is now here, financial markets have experienced increased volatility, reflecting investor apprehension about the potential economic impact of the impending tariffs.

Consumer confidence lowest

Consumer Confidence Sinks to a Four-Year Low: The Conference Board’s consumer confidence index (CCI) dropped sharply in February, declining by 7 points to 98.3. This marks the third consecutive month of decreases, as well as the largest monthly decline in the index since August 2021.

The index provides insight into how optimistic or pessimistic consumers are about the state of the economy in the near term. It includes outlooks on business conditions, the labor market, income prospects, the current and expected financial situation, and the likelihood of a recession.

Embrace for impact: beef up your emergency savings to avoid tapping your retirement savings

Now is a good time to beef up your emergency savings to cover at least 6 months to 2 years of expenses. With so much uncertainty and a likely weakening economy, having cash on hand provides a cushion against unforeseen financial blows, such as layoffs or other emergencies. It also helps you avoid tapping into retirement savings like 401(k) accounts. In general, it’s a bad idea to dip into investments when markets are in distress.

The ABCs of Roth Conversions: Backdoor, Mega Backdoor, and More

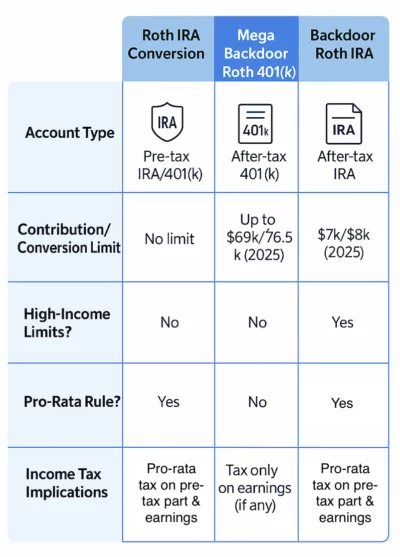

It’s tax time. Roth IRA and Roth 401(k) are very popular tax-sheltered vehicles. However, when terms like Roth IRA conversion, Mega Backdoor Roth 401(k) Conversion, and Backdoor Roth IRA Conversion are thrown around, people (including this author) are often confused. These strategies share the common goal of moving money into a Roth account for tax-free growth but differ significantly in execution, limits, and tax implications. Understanding them could help you make fewer mistakes (believe me, this author has made errors that complicated much of a tax filing). Let’s clarify each term and break down their key features.

1. Roth IRA Conversion

A Roth IRA conversion involves transferring funds from a pre-tax retirement account (like a Traditional IRA or 401(k)) into a Roth IRA. This is a straightforward process where you pay income taxes on the converted amount because the contributions were made with pre-tax dollars.

- Conversion Limits: There are no annual limits for Roth IRA conversions—you can convert as much of your pre-tax retirement savings as you want, provided you can cover the resulting tax bill.

- High-Income Considerations: There are no income limits for Roth IRA conversions, making this strategy accessible to high-income earners.

- Pro-Rata Rule: If you have both pre-tax and after-tax funds in IRAs, the Pro-Rata Rule applies. Taxes are calculated based on the ratio of pre-tax to total IRA balances.

- Income Tax: You’ll owe income tax on the entire converted amount since the funds were never taxed before.

2. Mega Backdoor Roth 401(k) Conversion

The Mega Backdoor Roth 401(k) Conversion is a powerful strategy for maximizing Roth contributions through an employer-sponsored 401(k) plan or a Solo 401(k). It allows for after-tax contributions beyond standard pre-tax limits, which are then converted to a Roth account.

- Contribution Limits: In 2025, the total contribution limit for a 401(k) is 69,000(76,500 for those aged 50+), which includes employee and employer contributions. After-tax contributions can make up the difference between pre-tax contributions and this cap.

- High-Income Considerations: There are no income limits for contributing to a 401(k), making this strategy particularly appealing for high-income earners.

- Pro-Rata Rule: This rule does not apply to 401(k) plans, as the after-tax contributions are tracked separately from pre-tax funds.

- Income Tax: Only earnings on the after-tax contributions are taxable if converted before they grow significantly.

3. Backdoor Roth IRA Conversion

The Backdoor Roth IRA Conversion is a workaround for high-income earners who exceed Roth IRA income limits. It involves making nondeductible after-tax contributions to a Traditional IRA and converting those funds to a Roth IRA.

- Contribution Limits: The maximum contribution to a Traditional IRA is 7,000(8,000 for those aged 50+) in 2025.

- High-Income Limits: For 2025, the ability to contribute directly to a Roth IRA phases out for single filers with modified adjusted gross income (MAGI) between 140,000 and 155,000, and for married couples filing jointly with MAGI between 228,000 and 238,000.

- Pro-Rata Rule: If you have other pre-tax IRA funds, the Pro-Rata Rule applies, meaning taxes are calculated based on the ratio of pre-tax to total IRA balances.

- Income Tax: If no pre-tax funds exist in your IRA, the conversion is typically tax-free since the contributions were made with after-tax dollars.

Infographic:

Below is a simplified infographic to help visualize the differences:

Summary

Simply put:

- Use a Roth IRA Conversion to move pre-tax retirement savings into a Roth account, with no income restrictions.

- Leverage a Mega Backdoor Roth 401(k) Conversion if you have access to a 401(k) plan that allows after-tax contributions—there are no income limits for this strategy.

- Opt for a Backdoor Roth IRA Conversion if you’re a high earner looking to bypass Roth IRA income limits (e.g., MAGI phase-outs for 2025).

For more information, refer to Roth IRAs and Roth 401(k).

Tools & Tips: Social Security Income Calculation Infographic

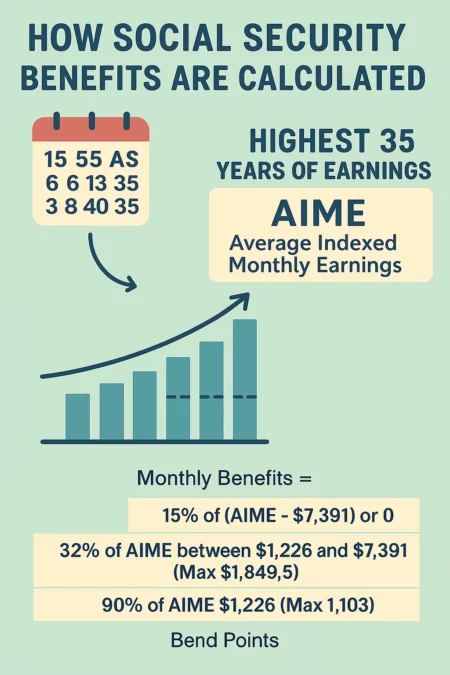

Another often confusing topic is how to calculate Social Security income. While you can use the Social Security website to get your estimated benefits, it’s still helpful to understand how that income is determined.

The following infographic illustrates the basic concept behind how Social Security Income is calculated:

Basically: the calculation is a two-step process:

- Step 1: Take your highest 35 years of earnings. If you haven’t worked for 35 years, the missing years will be counted as zero. Then, it calculates the so-called AIME (Average Indexed Monthly Earnings), which is essentially the average of your monthly earnings adjusted for inflation.

- Step 2: Use the bend points calculation to determine your monthly benefits. This is based on a tiered formula:

- 90% of the first $1,103 of AIME

- 32% of the amount between $1,103 and AIME if AIME is lower than $7,391, otherwise, would be 32%*(7391-1103)=1849.5

- 15% of any AIME above $7,391, or 0 if AIME is below this threshold.

Market Overview

The financial markets have been under stress as President Trump announced the so-called “reciprocal” tariff, which will become clearer in the coming days. Nevertheless, U.S. stocks are definitely in a downtrend. Whether this will develop into a full-blown bear market remains to be seen.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -1.5% | -6.2% | -6.3% | -2.2% | 7.5% | -1.7% |

| Foreign Stocks | -1.4% | 0.8% | 5.3% | -3.8% | 5.0% | 1.2% |

| US REITs | -0.5% | -4.4% | 1.2% | -7.2% | 5.8% | -1.0% |

| Emerging Market Stocks | -2.1% | 2.1% | 1.9% | -5.7% | 7.8% | 0.8% |

| Bonds | -0.2% | -0.5% | 1.8% | -1.9% | 3.3% | 0.5% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

At a time like this, we recommend reviewing your financial situation, beefing up emergency savings, and staying the course.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?