The Hidden Benefit of Emergency Savings Accounts: It’s a ‘Regular’ Savings Account with Free Employer Match

In this issue:

- Latest in Retirement Savings & Personal Finance

- One Percent Difference: Fees and Growth

- Asset Allocation Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance

Here is some of the latest news:

Target-Date Fund (TDF) Mess

Target-date funds (TDFs) have become prevalent in retirement plans, with many adopting them as default investment options. However, they are now under scrutiny due to concerns about their effectiveness and suitability for all investors:

- Vanguard fined: In December 2020, Vanguard reduced the minimum investment for its Institutional Target Retirement Funds from $100 million to $5 million. This change prompted many investors to transition from higher-cost Investor Target Retirement Funds to the lower-cost Institutional shares. However, this mass movement led to significant redemptions in the Investor funds, forcing them to sell assets to meet withdrawal demands. Consequently, remaining investors in these funds faced substantial capital gains distributions, resulting in unexpected tax liabilities. As a result, Vanguard was fined $106.4 million by the SEC and had to pay an additional $40 million to settle a related class-action lawsuit

- One size doesn’t fit all: People have different risk tolerances, so relying solely on age as a factor is not ideal. However, it’s still better than neglecting your investments for a long time. Those seeking more customization should first determine their risk tolerance using an asset allocation calculator (such as MyPlanIQ’s, discussed shortly) and, if needed, consult a financial planner. They can then build a portfolio using low-cost index funds (see Asset Allocation Portfolio Templates). However, this approach requires periodic reviews. If you’re unable to do that, target-date funds (TDFs) are still better than nothing.

- Lackluster returns: Another criticism of target-date funds (TDFs) is their underperformance. For example, Vanguard’s Target-Date 2040 Fund (VFORX) allocates 29% to international stocks and 7% to international bonds, both of which have significantly impacted its returns over the past decade.

- Volatility reduction: In recent years, rising inflation has led to falling intermediate-term bond prices, resulting in poor returns for target-date funds (TDFs), particularly for retirees or those nearing retirement. This has sparked criticism, highlighting the inflexibility of TDFs. Active investors can look for some tactical asset allocation portfolios like MyPlanIQ’s to help to reduce large drawdown and protect capital in a severe market downturn.

Annuities Become More Popular for Retirement Income

Annuities are gaining renewed popularity as a way to ensure guaranteed income in retirement. The key factors driving this trend include:

- High-Interest Rate Environment: Rising interest rates have increased annuity payout rates, making them more attractive to retirees.

- Recent market volatility: characterized by higher economic uncertainty and elevated stock market valuation levels, makes guaranteed annuity income a reasonable choice to avoid significant drawdowns when the next downturn occurs.

- Non-guaranteed pensions from defined-contribution 401(k) and 403(b) plans make it sensible to allocate a portion of funds to annuities for added protection.

However, it is crucial to understand the potentially high fees associated with annuities. If the terms seem too complicated or too good to be true, it may be best to avoid them.

The Hidden Benefit of Emergency Savings Accounts: It’s a ‘Regular’ Savings Account with Free Employer Match

Starting in 2024, employers can offer Emergency Savings Accounts (ESAs) linked to defined-contribution plans (e.g., 401(k)s). Employees can contribute up to $2,500 (or a lower employer-set cap) into these designated Roth accounts through payroll deductions. Withdrawals are tax-free and penalty-free, providing flexibility for unforeseen expenses like medical bills or car repairs. Furthermore, employers may also automatically enroll employees at a contribution rate capped at 3% of salary, with the option for employees to opt out or adjust their contributions.

Here, we explain that if your employer provides an ESA option, you should not opt out under any circumstances, even if you have an urgent need for cash. We will reveal a ‘hidden’ benefit of ESAs that essentially turns your ESA into a ‘regular’ savings account while earning free employer matching contributions.

Key ESA Features

- Contribution Limits: ESAs usually have a cap, often around $2,500 to $10,000, depending on the employer.

- Tied to Your 401(k): Contributions to your ESA are counted together with your regular 401(k) contributions toward the annual contribution limit of $23,500 in 2025. This means that the total amount you contribute to both accounts combined cannot exceed this limit.

- After-Tax Contributions: Unlike traditional 401(k) contributions, ESA contributions are made after tax, so withdrawals are tax-free. ESA is a Roth account.

Employer Matches Still Apply

One of the biggest advantages of an ESA is that your employer’s 401(k) match still applies to your contributions—even though your ESA itself isn’t part of your long-term retirement fund.

Example:

- Your employer offers a dollar-for-dollar match up to 5% of your salary.

- You earn $60,000 per year.

- Normally, you’d have to contribute $3,000 every month to your 401(k) to get the full match.

- However, if your ESA is part of the plan, contributions to your ESA count toward earning the match.

This means you can strategically allocate funds to your ESA without sacrificing employer-matched retirement contributions.

NOTE: beware that the employer match goes into your regular 401(k) account, not to the ESA account.

Flexible Withdrawals: No Restrictions on How You Use Your ESA

Unlike a 401(k), your ESA funds are not locked away for retirement. You can withdraw money at any time, but most plans allow only one withdrawal per calendar month.

- No penalty for withdrawals.

- No restrictions on how you spend the money.

- Funds remain liquid and accessible, just like a regular bank savings account.

This makes an ESA an attractive alternative to a traditional savings account—with the added bonus of employer-matched contributions.

For more details and an example, see this article.

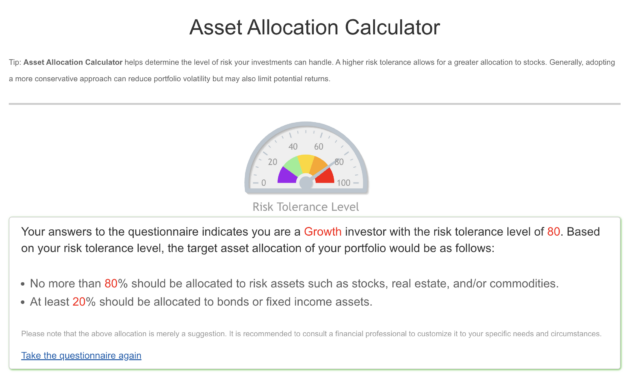

Tools & Tips: Asset Allocation or Risk Profile Calculators

When deciding how much risk you can tolerate in your retirement investments, you shouldn’t overlook the popular Bogleheads Wiki. If you prefer a straightforward question-and-answer format to help determine your risk tolerance, you can try our Asset Allocation Calculator.

The calculator asks questions in the following three categories:

- Time Horizon:

- Your investment time horizon influences how much risk you can afford to take.

- Longer horizons allow for higher allocations to stocks, as there’s more time to recover from market downturns.

- Shorter horizons typically require more conservative investments like bonds or cash equivalents to preserve capital.

- Risk Tolerance:

- Risk tolerance reflects your comfort with market volatility and potential losses.

- Tools like the Asset Allocation Calculator can assess this based on scenarios like market downturn reactions and return expectations.

- A higher risk tolerance permits a greater allocation to riskier assets like stocks, while a lower tolerance leans toward safer investments like bonds.

- Financial Stability:

- Stable income sources (e.g., salary, pension, rental income) enable higher exposure to riskier assets.

- Investors with uncertain or unstable incomes should prioritize a conservative portfolio to protect their principal.

It prompts you to answer five questions in the categories above to determine how much you should allocate to ‘risk’ assets, including stocks, high-yield bonds, real estate, and commodities.

The suggestion is merely an estimate. You should use other resources and/or consult financial advisors for a more accurate assessment if desired.

Market Overview

Economy-wise, last week, we saw that the U.S. economy added only 143,000 jobs in January, a slowdown from December’s gain of 307,000 jobs. However, the unemployment rate declined to 4.0%. Normally, the report could be characterized as a bit weak labor market.

On the other hand, the January 2025 jobs report also revealed that wages increased by 0.5% month-over-month, translating to an average hourly earnings rise of $0.17 to $35.87. On a year-over-year basis, wages grew by 4.1%, exceeding economists’ expectations of 3.8% and maintaining strong momentum from December’s annual growth rate of 3.9%. Overall, this signals a still tight labor market and a likely elevated inflation.

The following table shows the major asset price returns, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -0.2% | 3.5% | 0.8% | 13.4% | 21.3% | 7.8% |

| Foreign Stocks | 0.7% | 5.4% | -1.3% | 3.0% | 8.5% | 3.3% |

| US REITs | 1.1% | 7.0% | -4.5% | 1.4% | 11.6% | 3.3% |

| Emerging Market Stocks | 1.2% | 4.6% | -4.5% | 3.0% | 11.4% | 3.1% |

| Bonds | 0.2% | 1.6% | -0.7% | -0.9% | 3.0% | 0.6% |

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?