Investing Can Feel Overwhelming — But There Are Easier Paths

For retirement plan participants (401(k), 403(b), etc.) who have no experience or very little experience in investing, putting money into a 401(k) account might feel overwhelming — especially for those who are completely new. However, many 401(k) plans these days do offer a few choices that can ease this anxiety.

One of the approaches widely adopted is the so-called one-fund approach. And the one-fund approach can have two types.

Target Date Funds: Set It and Forget It

The first is the so-called target fund. Basically, it’s as simple as finding out when you plan to retire. For example, let’s say you expect to retire in 2050 — then you go look at your 401(k) plan’s investment options and find the closest fund to that year. Usually, these target date funds come in five-year gaps: like a Target Date Fund 2030, Target Date Fund 2035, Target Date Fund 2050, and so on.

You just find the closest one. You can scale down if you feel more conservative, or if you think you’ll retire a bit later, pick the one above it. Once you pick it — that’s it. Fire and forget.

What these funds do is gradually adjust over time, based on what’s called a gliding path approach. They automatically reduce stock exposure as you get closer to retirement — because stocks are generally much more volatile than bonds. It’s prudent to reduce stock exposure as you near the time when you’ll need the money.

So by the time you’re actually at retirement — say, you chose a 2045 fund and now it’s 2045 — the fund’s stock exposure might have already come down to around 50%, with the rest in bonds. It gives you peace of mind. You don’t have to worry about which stocks or bonds you should hold.

Furthermore, it also automatically balances things out. Among stocks, for example, the fund may hold a majority in U.S. stocks, but also some international or even emerging market stocks. Again — you don’t need to think about that. The fund takes care of it.

That’s the first approach.

Balanced Funds: Another Simple Choice

The second approach is — if your plan doesn’t have these target date funds available — to see if your plan offers a so-called balanced fund.

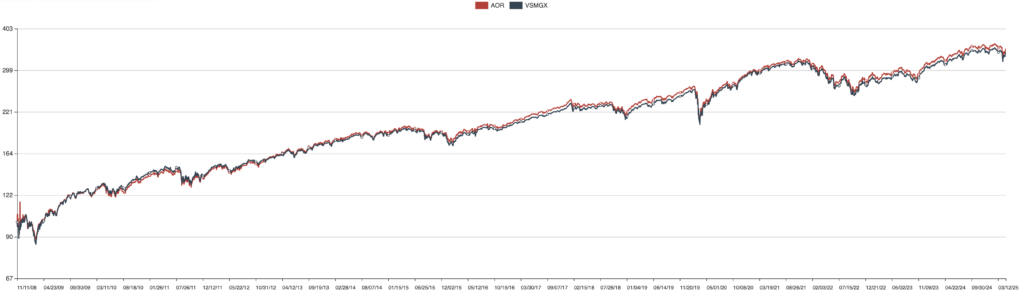

There’s been a lot of research and discussion, by both academics and people like Bogleheads, suggesting that simply choosing a balanced fund — typically something like 60% stocks and 40% bonds — can work really well. Examples would be something like VSMGX (VANGUARD LIFESTRATEGY MODERATE GROWTH FUND INVESTOR SHARES) or AOR (iShares Core Growth Allocation ETF). These funds maintain a steady mix of stocks and bonds (e.g., 60% stocks, 40% bonds).

The following are the holdings of the two funds as of March 31,2025:

Vanguard LifeStrategy Moderate Growth Fund (VSMGX)

Asset Allocation (as of March 2025)

| Asset Class | Allocation |

|---|---|

| U.S. Stocks | 36.2% |

| International Stocks | 24.5% |

| U.S. Bonds | 26.9% |

| International Bonds | 11.8% |

| Cash | 0.6% |

| Total | 100% |

iShares Core Growth Allocation ETF (AOR)

Asset Allocation (as of March 2024)

| Asset Class | Allocation |

|---|---|

| U.S. Large-Cap Stocks | 31% |

| U.S. Mid/Small-Cap Stocks | 3% |

| Developed Markets ex-U.S. | 20% |

| Emerging Markets | 7% |

| U.S. Bonds | 33% |

| International Bonds | 6% |

| Total | 100% |

Their returns are also very comparable:

And if you choose this type of 60/40 fund, it can actually work wonders. No matter where the market is — bull or bear — because when you are in the accumulation phase, you are consistently contributing from your paycheck, month after month, year after year.

Some of your contributions will happen at the bull market peaks. Some will happen during bear market lows. When you invest at a bull market peak — during very speculative times — it might take a longer time for your money to achieve good long-term returns. That’s intuitive, right? Because if you invest when stocks are expensive, it naturally takes time for the growth to catch up. And it also exposes you to bigger interim losses if a bear market hits.

So even though it might feel too steady — maybe even a little boring — a 60% stock / 40% bond balanced fund can actually do the job fairly well.

Of course, this depends on how the years unfold. If you start investing during a long bull market and then experience a deep bear market (or even a secular bear market), it might take 15 to 20 years just to get back to your original investment level.

And in that sense, a balanced fund can give you an edge — both in terms of managing volatility and even achieving respectable returns.

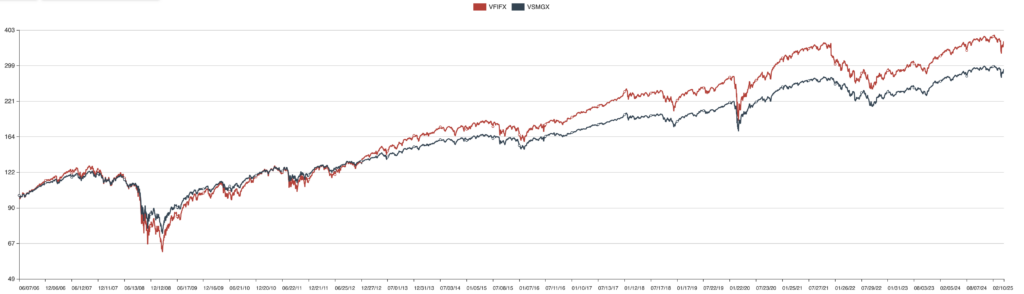

The following chart compares the returen of VFIFX (VANGUARD TARGET RETIREMENT 2050 FUND INVESTOR SHARES) and VSMGX. You can see that VSMGX has had smaller interim loss (also known as drawdown) during bear markets like the 2008 and 2020 ones. But that comes with a lower overal return, which should be expected as it has smaller exposure in stocks.

Summary

Investing, especially at the beginning, often feels like stepping into a fog. So many funds. So many opinions. Everyone seems to have a different answer, and most of them sound either too complicated or too confident. You hear about risk tolerance, asset classes, tax efficiency — and then you end up doing nothing at all. Or worse, chasing something shiny.

That’s why the idea of a One-Fund Portfolio is kind of refreshing. It doesn’t try to impress you with complexity. It just gives you a way to start — with something solid, diversified, and aligned with the basic truths of long-term investing.

Usually, we’re talking about a total market index fund. Or a target-date retirement fund. Either way, the point is: one fund, low cost, globally diversified, automatically rebalanced. No constant tinkering. No decision fatigue.

Is it perfect? No, of course not. But that’s not the goal. The goal is to get started — in a way that avoids big mistakes and leaves room for learning over time. And honestly, for most people, that’s already a huge win.

Remember, the best portfolio is the one you can stick with. For more details, explore the original Bogleheads discussion.