The Right Way to Withdraw from Your 401(k) Without Regret

In this issue:

- Latest in Retirement Savings & Personal Finance: $1.5 Million’s Retirement Mileage Across Various States, Therapy Needed in Market Turmoil

- The Right Way to Withdraw from Your 401(k) Without Regret

- Credit Card Debt Consolidation Calculator

- Market Overview

Latest in Retirement Savings & Personal Finance: $1.5 Million’s Retirement Mileage Across Various States, Therapy Needed in Market Turmoil

$1.5 Million’s Retirement Mileage Across Various States

Based on a Northwestern Mutual survey, Americans consider roughly $1.46 million the magic number for a reasonable retirement life. Based on this, the mileage can vary dramatically.

- 1. West Virginia: $1.5 million will last 54 years

- 2. Kansas: $1.5 million will last 52 years

- …

- 26. Illinois: $1.5 million will last 44 years

- 34. Florida: $1.5 million will last 39 years

- …

- 48. California: $1.5 million will last 24 years

- 49. Massachusetts: $1.5 million will last 23 years

- 50 Hawaii: $1.5 million will last 17 years

Well, the weather (in Hawaii and California) and culture (in Massachusetts) are that costly. Retiring in West Virginia could last you three times longer than in Hawaii!

Therapists Needed in Market Turmoil

Recent market turmoil amid the tensions of government restructuring, tariffs, and geopolitical issues is making noise on social media platforms like Reddit. Some people are panicking about the loss of their retirement savings. Similarly, financial planners are receiving more and more calls for guidance on how to deal with the financial losses of their clients. If you experience anxiety, we believe it’s very helpful to actively seek counseling and support. Both Reddit communities, such as r/Retirement401k, and financial advisors/planners, if you have one, can be beneficial. People on Reddit, for example, are often eager to help. Sometimes, just receiving reminders from others is more useful than taking actions such as selling in a panic! Our advice: stay the course.

Rising Credit Card Debt Burden for Adults Aged 50 and Older

Based on an AARP report, nearly half of adults aged 50 and older owe $5,000 or more in credit card debt, and 28% carry a balance of $10,000 or more. For these people, most roll over their credit card balances from month to month. Many only make the minimum payment on their credit cards, which can have interest rates as high as 20%! This situation has become a serious problem, leading many to resort to using their retirement savings to pay off their debts. In fact, when people reflect on their biggest regrets after retirement, the most common one is retiring with too much debt.

The Right Way to Withdraw from Your 401(k) Without Regret

We understand that in various situations, people need to tap their retirement savings for emergency needs. In the following, we will tell you the correct order of considering options if you indeed want to pursue this route. However, before going into this, as always, we want to emphasize that you should try to consider other resources, such as debt consolidation or equity loans, first. In principle, they should be considered even before thinking about taking money from your retirement accounts.

Hardship withdrawals are generally allowed only for “heavy and immediate” financial needs, and these are pretty strictly defined by the IRS. Medical expenses can sometimes qualify, but it usually needs to be for yourself, your spouse, or your dependents. Hardship withdrawals do not come with any penalty though you still need to pay income tax for the withdrawl. Whether getting dental work done in Spain would qualify might be tricky, and you’d need to check the specifics of your 401(k) plan. If your HR approves this as ‘hardship’, it might be OK. This should be the first option to consider if you need money from your 401(k) retirement account.

A 401(k) loan might be an option if your plan allows it. The cool thing about a loan is that you’re essentially borrowing from yourself, and the interest you pay goes back into your 401(k). You can generally borrow up to $50,000 or 50% of your vested account balance, whichever is less [0]. You’ll need to make regular payments, usually through payroll deductions. Just remember, if you leave your job, you’ll likely have to repay the loan pretty quickly, or it’ll be considered a withdrawal, and you’ll face those taxes and penalties. This should be the second option to consider.

Early withdrawals, in general, are possible, but they come with a cost. You’ll typically have to pay income tax on the amount you withdraw, and if you’re under 59 1/2, you’ll likely get hit with a 10% penalty from the IRS. So, taking out $4,000 could end up costing you quite a bit more after taxes and penalties. This should be the last option to consider.

Important Note: It’s often debated whether a 401(k) hardship withdrawal or a 401(k) loan is the better option. If you have the ability to repay the loan over time, taking a 401(k) loan is generally preferable. This is because repaying the loan allows you to restore your retirement savings, whereas a hardship withdrawal permanently reduces your retirement balance. Additionally, a hardship withdrawal is subject to income tax, whereas a loan is not—helping you avoid an immediate tax burden.

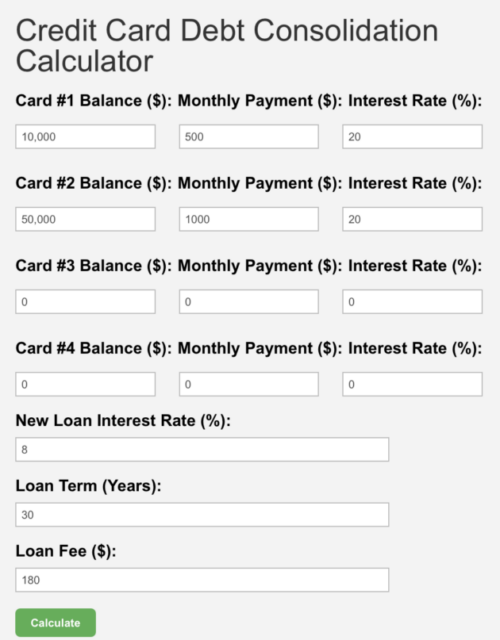

Tools & Tips: Credit Card Debt Consolidation Calculator

Speaking of credit card debt burdens to adults 50 years and older, we believe it’s extremely important to consolidate credit card debts if you happen to have much. The Credit Card Debt Consolidation Calculator helps you evaluate how consolidating your credit card debts into a single, lower-interest loan can reduce your monthly payments and total interest costs. By entering your current credit card balances, monthly payments, interest rates, and details of a potential consolidation loan, you can instantly see the potential savings and repayment timeline.

The following shows the calculator’s inputs and outputs:

As stated in the Credit Card Debt Consolidation Calculator, the ultra-high interest rates from credit cards, often ranging from 15% to 28%, can quickly cause debts to spiral out of control, creating a huge burden for individuals and sometimes leading to personal bankruptcy. It is widely recognized that one should first tackle this type of debt, and, if possible, consolidate it using other loans such as home equity loans, personal loans, or even 401(k) loans. This calculator should help people understand why pursuing consolidation can be so much better.

Market Overview

Last week saw the continous stock market weakness amid the following main developments:

- Employment: February’s job gains came in at 151,000, slightly below expectations but higher than January’s adjusted figure of 125,000. The overall trend shows moderating job growth.

- Trade tensions: The U.S. imposed 25% tariffs on most goods from Canada and Mexico, while also increasing duties on Chinese imports. This led to retaliatory measures from these trading partners, though some tariffs were later suspended for a month. The other bickering nonsense is that the US kept making noises about annexing Canada and Greenland, stirring up hostile sentiment. This is totally uncalled for, in our opinion.

- Interestingly, the Atlanta Fed revised its GDPNow forecast for Q1 2025 by introducing a gold-adjusted approach that eliminates gold from imports and exports, as the recent surge in imports has negatively impacted its GDPNow estimate. By doing so, for example, on March 7, after a positive jobs report, the gold-adjusted GDPNow improved to 0.4% annualized growth, while the headline reading still showed contraction at -1.6%. At this moment, it’s likely the GDPNow forecast is still in positive territory.

The following table shows the major asset price returns and their trend scores, as of last Friday:

| Asset Class | 1 Weeks | 4 Weeks | 13 Weeks | 26 Weeks | 52 Weeks | Trend Score |

|---|---|---|---|---|---|---|

| US Stocks | -2.2% | -7.7% | -6.5% | 0.8% | 11.5% | -0.8% |

| Foreign Stocks | -0.6% | 1.0% | 2.7% | 1.9% | 7.8% | 2.6% |

| US REITs | -2.5% | -1.6% | -3.9% | -7.8% | 8.8% | -1.4% |

| Emerging Market Stocks | 3.7% | 1.8% | 0.3% | 4.3% | 11.7% | 4.4% |

| Bonds | -0.1% | 0.6% | 0.4% | -2.4% | 4.1% | 0.5% |

More detailed returns and trend scores can be found on MyPlanIQ.com Market Overview.

At the moment, stocks have entered a correction phase (the S&P 500 has dropped 10% from its peak). Whether this will sustain or bounce back in the coming weeks is crucial for understanding the intermediate trends in financial markets. In any case, we advocate staying the course.

Struggling to Select Investments for Your 401(k), IRA, or Brokerage Accounts?