-

2026 Tax Season Begins Today

- Latest in Retirement Savings & Personal Finance

- 2026 Tax Season Begins Today

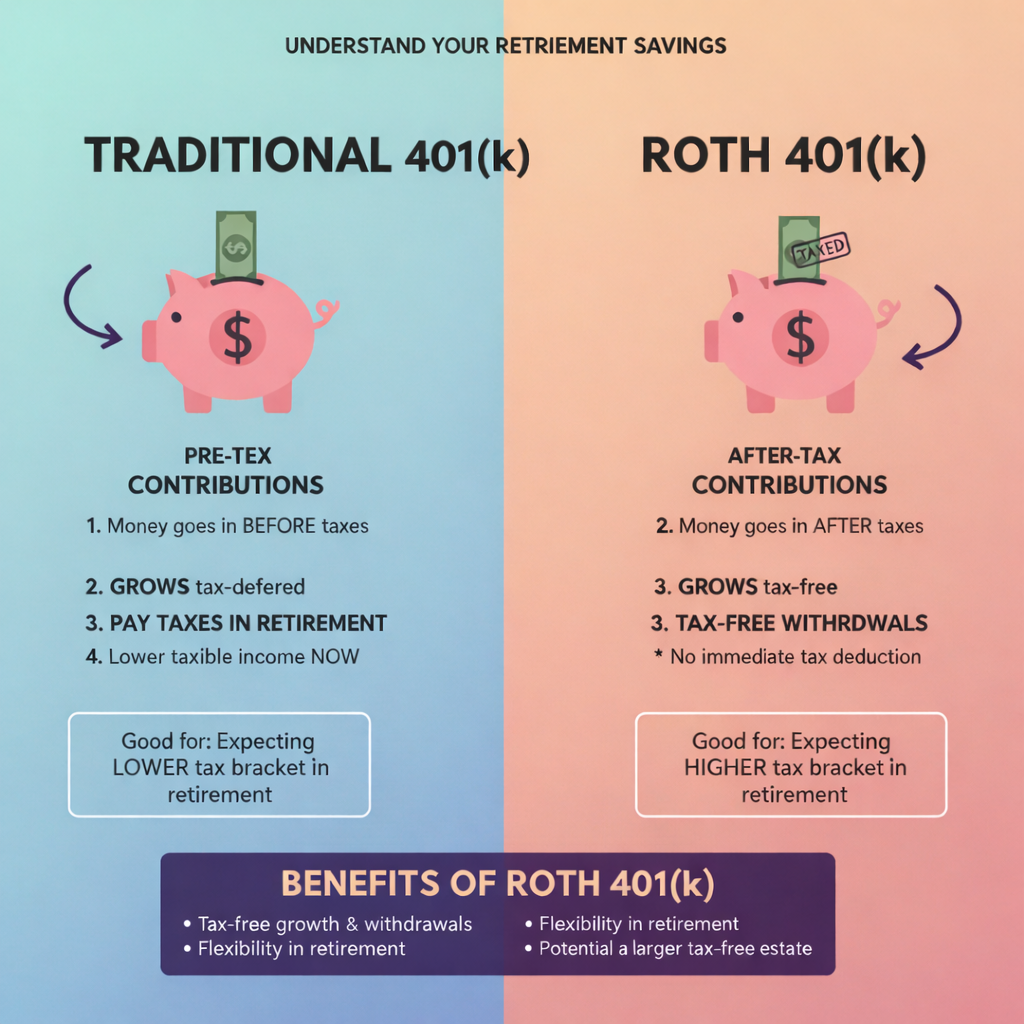

- Tools & Tips: Traditional 401(K) vs. Roth 401(K)

- Market Overview

-

Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Latest in Retirement Savings & Personal Finance

- Useful Tips for 401(k)s, IRAs, and RMDs in the New Year

- Tools & Tips: Roth IRA Compounding

- Market Overview

-

The $7,000 Roth IRA Myth, Why It Is a Bigger Deal Than People Think

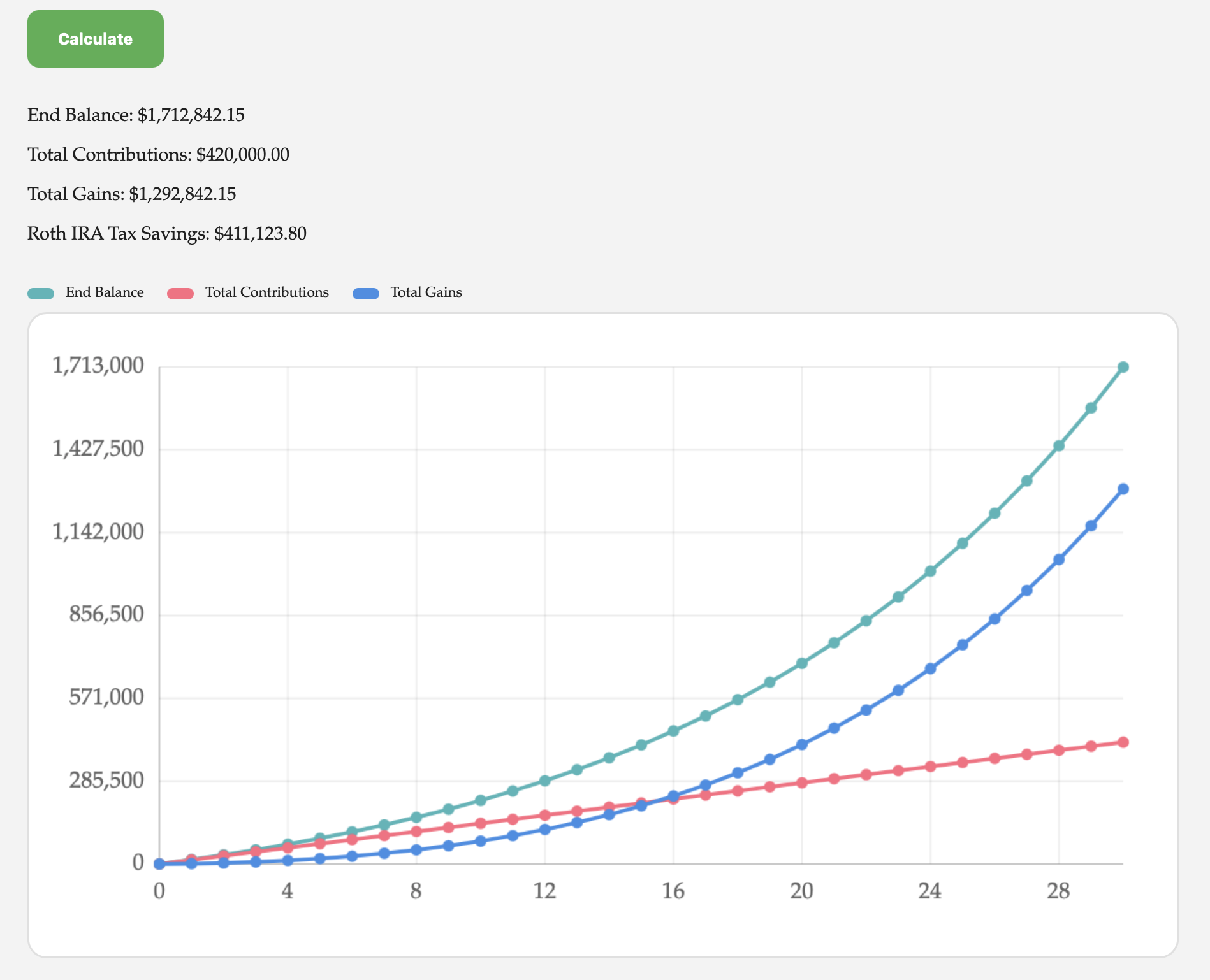

Many people look at the $7,000 annual Roth IRA limit and immediately dismiss it. Too small, not impactful, not worth the hassle. Big mistake! Let’s use a simple example. A husband and wife each contribute $7,000 a year, so $14,000 total, from age 30 to 60. That is 30 years of steady investing at an assumed 8 percent return. Total contributions come to $420,000. By age 60, that Roth balance grows to about $1.6 million. Roughly $1.16 million of that is pure growth, and it comes out tax free. If you live in a no state tax environment, you just avoided federal long term capital gains and the extra 3.8 percent surtax on investment income, already a meaningful number. Now layer in a high tax state. At an 8 percent state tax rate, that same $1.16 million of gains would have faced another large haircut (actually like $411K tax savings). The Roth just simply protects such a big chunk of your gain. The following are results from our Investment Return Calculator: And it does not stop there. Most people do not touch Roth money first. They let it keep compounding while spending from pre tax or taxable accounts. Let that same Roth grow another 10 years, untouched, at the same 8 percent. By age 70, it is worth roughly $3.9 million. Now you are looking at close to $3.3 million of gains that will never be taxed. In a zero state tax scenario, that already avoids a large federal tax bill. In an 8 percent state tax scenario, the difference becomes even more dramatic: a $1 million savings. This is where people underestimate the impact. The contribution feels small. The tax free compounding over decades is not. This is real money, not theoretical. High income earners often respond with another objection. Fine, but my income is too high to contribute to a Roth IRA anyway. Not really. This is where the backdoor Roth comes in. The process is simple in concept. You contribute to a traditional IRA using after tax dollars, since there is no income limit on contributions. Then you convert that contribution to a Roth IRA. If done correctly and promptly, there is little to no tax cost. The key rule is that you cannot have other pre tax IRA balances sitting around, including SEP or SIMPLE IRAs, or the conversion becomes partially taxable. Many people solve this by rolling old IRAs into a 401(k) first. Once set up, this becomes a repeatable annual process. So the real question is not whether the Roth is too small to matter. It is whether you want to keep paying taxes on millions of dollars of future growth, or quietly opt out while you still can.

-

Ultimate 2026 Retirement Playbook for 401(k)s & IRAs

Extremely use tips to maximizing 401(k) match, RMDs and IRA tactics

-

New Year Resolutions for Your Personal Finance

- Latest in Retirement Savings & Personal Finance

- New Year Resolutions for Your Personal Finance

- MyPlanIQ 2026 Market Outlook

-

January 2026 MyPlanIQ Portfolio Update

- Portfolios: 2025 Recap

- Interesting Funds Review

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

Main 2026 Tax Changes for Your Benefits

Several federal tax updates take effect in 2026, driven by the IRS annual inflation adjustments and provisions tied to the “One Big, Beautiful Bill Act”. These changes generally raise thresholds and deductions

-

2025 Crystal Ball Market Prediction Scorecard

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

2025 Wall Street Crystal Ball Scorecard

2025 Wall Street Crystal Ball Scorecard (So Far): Why Forecasting Is Not A Strategy As we are now only two weeks to the end of 2025 and many Wall Street analysts have started to put forward a new year 2026 predictions, it’s a good time to look at how these popular financial professionals have performed up to now. Where we stand (so far): The dataset I’m scoring To keep this objective, I used a single, clean prediction type: 2025 year-end S&P 500 targets. A Bloomberg-sourced table (compiled and published by Fundstrat on Dec 10, 2024) included 23 strategist targets, ranging from 4,450 to 7,100. Scoring method: absolute % error vs 6,827.41 (Dec 12 level). (Yes, the final “grade” can still change by Dec 31—but the main conclusion is already visible.) The tallies: how accurate were they? Closest calls (so far) Biggest misses (so far) The more important point: forecasts didn’t just miss—they moved Even if a target ends up “close,” the path matters—because most investors don’t hold steady when headlines get loud. Example: In April 2025, multiple firms cut targets sharply amid tariff/trade-war turmoil: Later, some targets re-inflated. For example, Oppenheimer raised back to 7,100 by late July 2025 after previously cutting to 5,950. What to do with this? What we can see are as follows: What we really need: a systematic strategy A systematic sound and intuitive strategy that our investments should adhere to year in and year out. MyPlanIQ has provided both Strategic and Tactical Strategies for decades (see Asset Allocation Strategy White Paper). For example, the following is the outline of a Strategic Asset Allocation (SAA) Of course, you can also allocate part of your investments to a tactical asset allocation portfolio that could avoid large drawdown or loss by dynamically changing stock and bond allocations based on prevailing market and economy conditions.

-

Personal Finance Year End Check List

- Latest in Retirement Savings & Personal Finance

- Personal Finance Year End Check List

- Tools & Tips: 12% Tax Bracket Is the Sweet Spot for Roth IRA Conversion

- Market Overview

-

How A Valuation Driven Bear Market Looks Like

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

December 2025 MyPlanIQ Portfolio Update

- Earnings, Recessions and Tech Stock Bubbles

- Value and Growth Funds Performance in a Valuation Compression Bear Market

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

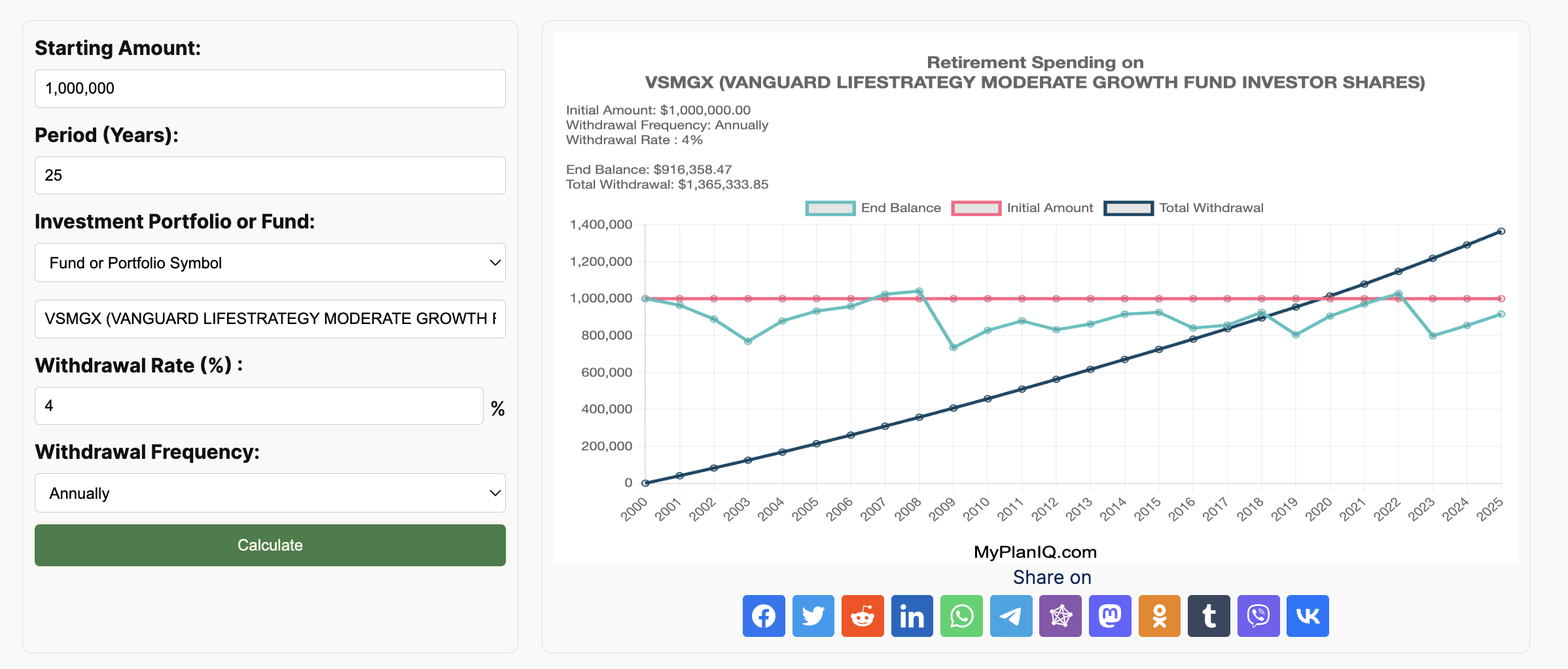

Stock Market Bubble & Retirement Savings

- Latest in Retirement Savings & Personal Finance

- Stock Market Bubble & Retirement Savings

- Tools & Tips: Retirement Spending Calculator

- Market Overview

-

Retirement Savings To Help Student Loan Payments

- Latest in Retirement Savings & Personal Finance

- Retirement Savings To Help Student Loan Payments

- Tools & Tips: I-Bond Comparison Calculator

- Market Overview

-

Retirement Plan Contribution Limits in 2026

Comprehensive retirement plans (401(k), 403(b, 457(b), Solo 401(k), SEP IRA, SIMPLE IRA, IRA, Roth IRA, TSP, HSA etc.) contribution limits for 2026

-

How Retirement Savings Can Quietly Reduce Your Student Loan Payments

Increasing Retirement Savings such as 401(k) can help reduce your monthly student repayment if you are on the federal IBR program. But

-

Series I Savings Bonds: Good Time to Buy?

- Latest in Retirement Savings & Personal Finance

- Series I Savings Bonds: Good Time to Buy?

- Tools & Tips: I-Bond Calculator

- Market Overview

-

Series I Savings Bonds: A Decent Shelter Against Inflation (If You Understand the Fine Print)

Is it worth to buy Series I Savings Bonds (I Bonds)? This article discusses what I Bond is and how it’s compared with money market and Inflation-Protected Securities (TIPs).

-

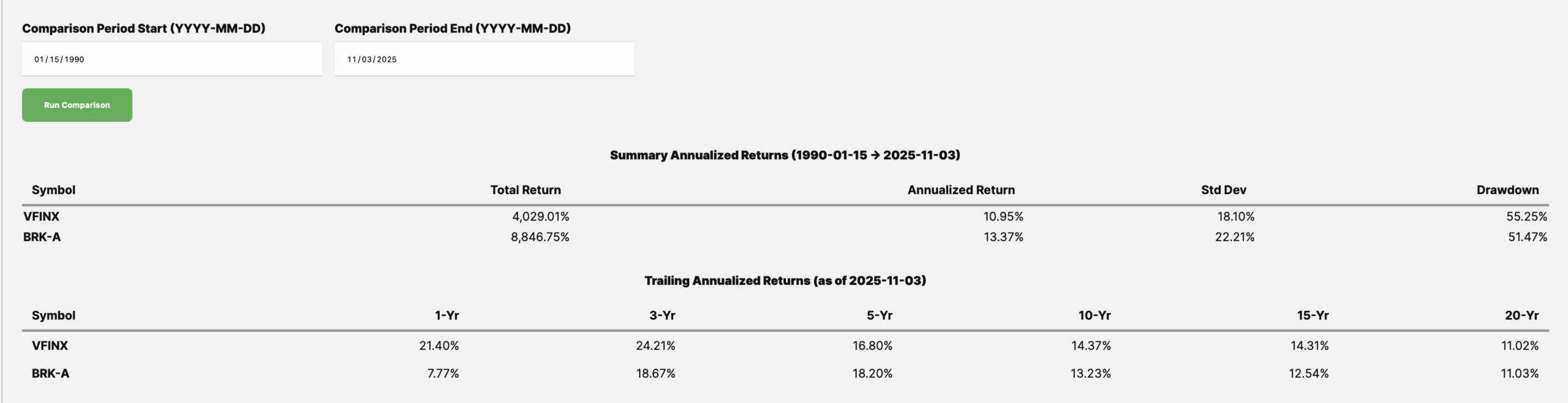

Super Businesses, Super Stocks

- Latest in Retirement Savings & Personal Finance

- Super Businesses, Super Stocks

- Tools & Tips: Return Comparison Calculator

- Market Overview

-

Super Stock List for 2025

Superior businesses with wide moats can have a very long runway. Their stocks reflect their business strength in the long run. We list super stocks for the various periods including up to last 50 years.