-

November 2025 MyPlanIQ Portfolio Update

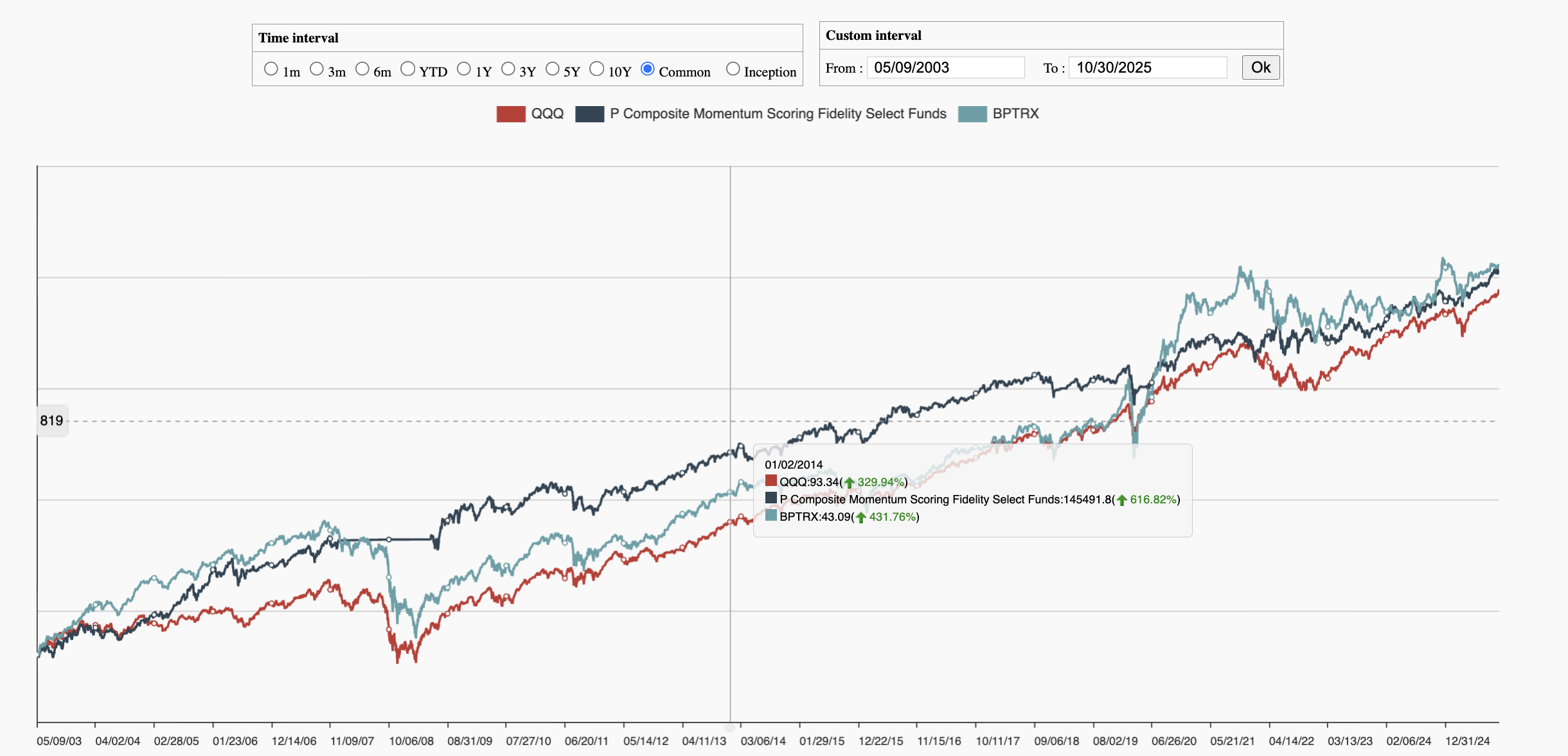

- Fidelity Select Industry Rotation Portfolio Review

- Top Performing Industries

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

2024 Millionaire Retirement Plans

- Latest in Retirement Savings & Personal Finance

- 2024 Millionaire Retirement Plans

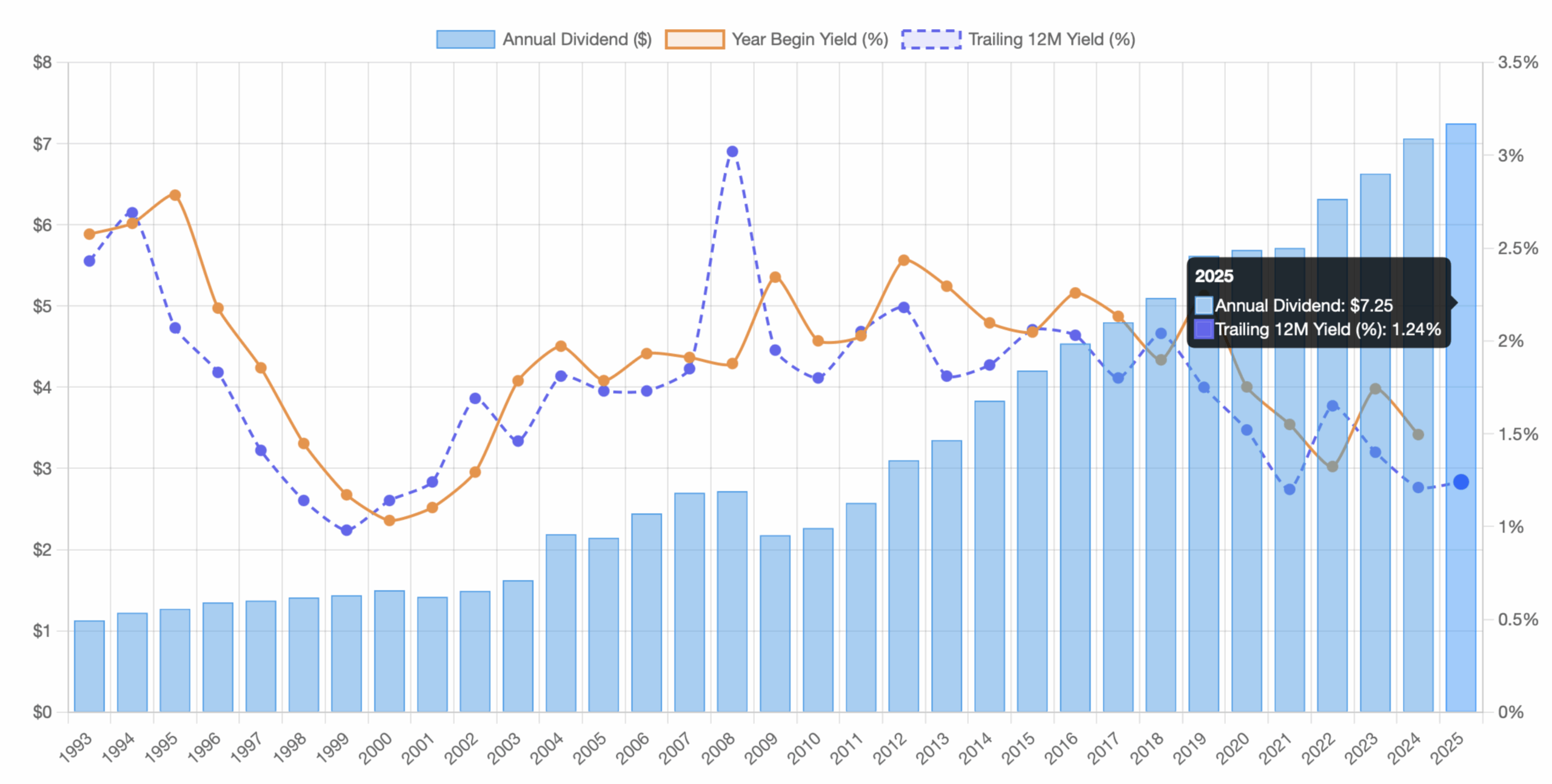

- Tools & Tips: Historical Stock Dividend Yield Chart

- Market Overview

-

The Quiet Millionaires of 2024: What Sets These Retirement Plans Apart

Every year, when new 401(k) data is released, it quietly reveals how uneven wealth building can be. In 2024, that picture is especially clear. The retirement plans with the highest average balances mostly belong to two types of organizations. On one side are high-income professionals such as physicians, lawyers, and boutique asset managers. These groups tend to have both strong personal contributions and large employer matches, often tied to firm profits. On the other side, a few large corporations, such as Texas Instruments and General Re, show that slow and steady saving across decades can also create significant wealth. MyPlanIQ recently did a study on all year 2024 retirement plans. We identified the top retirement plans that have the highest average participant account value. We limited our study in plans that have at least 100 participants. Below is a summary of the top 37 retirement plans by average account value. The numbers speak for themselves. Rank Retirement Plan Sponsor Average Account Value 1 Lone Pine Capital LLC 401(k) Profit Sharing Plan Lone Pine Capital LLC $1,612,021 2 Anesthesia Service Medical Group, Inc. 401(k) Profit Sharing Plan Trust Anesthesia Service Medical Group, Inc. $1,240,779 3 Medical Center Emergency Services Retirement Savings Thrift Plan Medical Center Emergency Services $1,217,978 4 Crescent River Port Pilots’ Association 401(k) Retirement Plan Crescent River Port Pilots’ Association $1,172,843 5 Irell & Manella Profit Sharing Plan Irell & Manella LLP $1,003,150 6 Anesthesia Consultants of Indianapolis, LLC 401(k) Profit Sharing Plan Anesthesia Consultants of Indianapolis, LLC $975,046 7 Fond du Lac Regional Clinic, S.C. 401(k) Profit Sharing Plan Fond du Lac Regional Clinic, S.C. $967,649 8 Wasatch Advisors, LP Deferred Profit Sharing Plan and Trust Wasatch Advisors, LP $924,154 9 Dodge & Cox Profit Sharing Plan Dodge & Cox $912,271 10 National Exchange Carrier Association Retirement Savings Plan National Exchange Carrier Association, Inc. $893,253 11 TI 401(k) Savings Plan Texas Instruments Incorporated $882,313 12 Employee Savings and Stock Ownership Plan of General Re Corp and its Domestic Subsidiaries General Re Corporation $862,746 13 Kleinberg, Kaplan, Wolff & Cohen, P.C. 401(k) Profit Sharing Plan Kleinberg, Kaplan, Wolff & Cohen, P.C. $860,649 14 Zeta Associates Incorporated Savings Plan Zeta Associates $829,709 15 Anesthesia Consultants of Indianapolis, LLC 401(k) Profit Sharing Plan Anesthesia Consultants of Indianapolis, LLC $804,322 16 Jennison Associates Savings Plan Jennison Associates LLC $797,881 17 Nutter, McClennen & Fish, LLP Lawyers Retirement Plan Nutter, McClennen & Fish, LLP $792,777 18 Carter Ledyard & Milburn LLP 401(k) Retirement Plan Carter Ledyard & Milburn LLP $778,761 19 Medical Anesthesia Group, P.A. Profit Sharing Plan Medical Anesthesia Group, P.A. $754,092 20 Bayerische Landesbank NY Employees Retirement Plan Bayerische Landesbank $747,774 21 Barrow, Hanley Profit Sharing & 401(k) Plan Barrow, Hanley, Mewhinney and Strauss, LLC $736,341 22 Callan LLC Retirement Savings Plan Callan LLC $717,465 23 Sills Cummis & Gross P.C. Defined Contribution Plan Sills Cummis & Gross P.C. $716,205 24 Maverick Capital, Ltd. 401(k) Plan Maverick Capital, Ltd. $676,958 25 Progressive Physician Associates, Inc. Retirement Savings Plan Progressive Physician Associates, Inc. $669,937 26 Jeffer Mangels Butler & Mitchell LLP Profit Sharing and 401(k) Plan Jeffer Mangels Butler & Mitchell LLP $663,531 27 QRM 401(k) Retirement Savings Plan Quantitative Risk Management, Inc. $662,045 28 Neuberger Berman Group 401(k) Plan Neuberger Berman Group LLC $661,047 29 MBIA Inc. Employees Pension Plan MBIA Inc. $658,502 30 Maher Terminals LLC Profit Sharing and 401(k) Plan Maher Terminals LLC $657,996 31 Willcox & Savage, P.C. Profit-Sharing Retirement Plan Willcox & Savage, P.C. $647,756 32 Morris, Nichols, Arsht & Tunnell LLP 401(k) Profit Sharing Plan Morris, Nichols, Arsht & Tunnell LLP $647,520 33 Eastman & Smith Ltd. Profit Sharing and Savings Plan and Trust Eastman & Smith Ltd. $643,627 34 APG Asset Management 401(k) Plan APG Asset Management $642,912 35 American Radiology Associates, P.A. Retirement Plan American Radiology Associates, P.A. $638,273 36 First Manhattan 401(k) Plan FMC Group Holdings LP $636,751 37 Downs Rachlin Martin Retirement Plan Downs Rachlin Martin PLLC $632,968 Across these 37 plans, the average account value stands close to $820,000, with a median around $754,000. That is a striking contrast to the national average, which remains under $120,000 for most retirement savers. The first major reason for this difference is compensation. These are high-income groups with the ability to contribute the annual maximum without hardship. Employers in these professional partnerships also tend to make hefty profit-sharing contributions. A doctor earning $400,000 a year or a law partner receiving a share of firm profits can easily reach contribution limits and still receive matching or profit-based additions on top. Over time, that combination of high base income and rich employer match drives account values far above what traditional salaried workers can achieve. The second reason is less about pay and more about time. Companies such as Texas Instruments and General Re demonstrate the quiet power of long-term consistency. Their plans have thousands of participants and more modest individual incomes, yet decades of continuous contributions and steady investment returns have compounded into substantial balances. The difference is discipline rather than income level. These two factors together explain why some retirement plans have reached the million-dollar mark while others lag far behind. High income and employer generosity create the initial lift. Long time horizons finish the job. In a period when many Americans are struggling to save even a fraction of what they will need, these plans are reminders that structure and time still matter more than luck. The quiet millionaires of 2024 did not chase returns or time markets. They simply contributed, matched, and waited long enough for patience to pay.

-

Last Quarter Checklist for 2025

- Latest in Retirement Savings & Personal Finance: All the Glittering Gold, Highest Household Credit Card Debt, More PE Funds Than McDonald’s

- Last Quarter Checklist for 2025

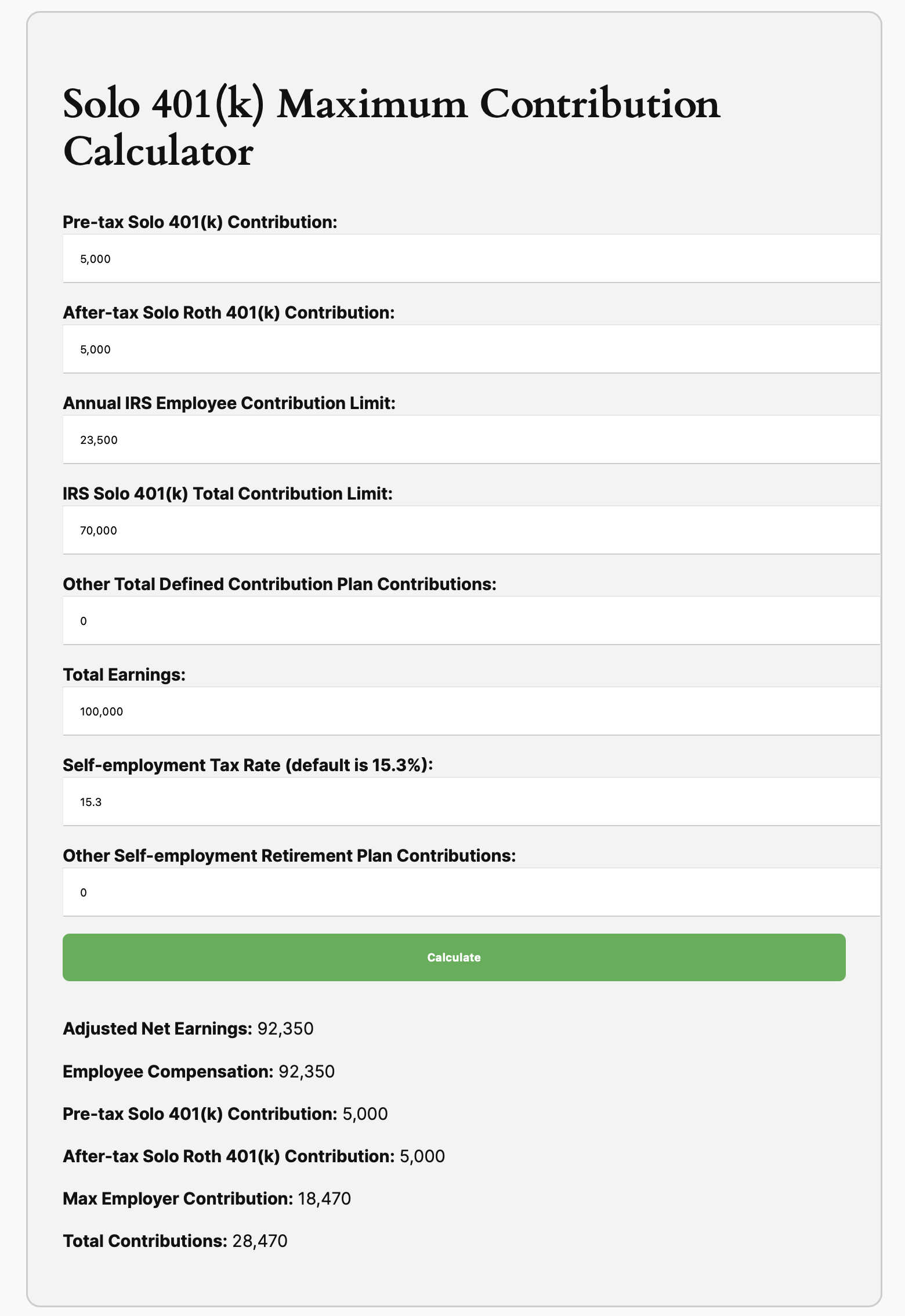

- Tools & Tips: Solo 401(k) Maximum Contribution Calculator

- Market Overview

-

Which Health Insurance Plan Is Better: HMO, PPO or HDHP?

- Latest in Retirement Savings & Personal Finance: Highest Health Benefit Cost in 15 Years, Visualize Americans’ Healthcare Affordability, Americans Admire Luxury Spending

- Which Helath Insurance Plan Is Better: HMO, PPO or HDHP?

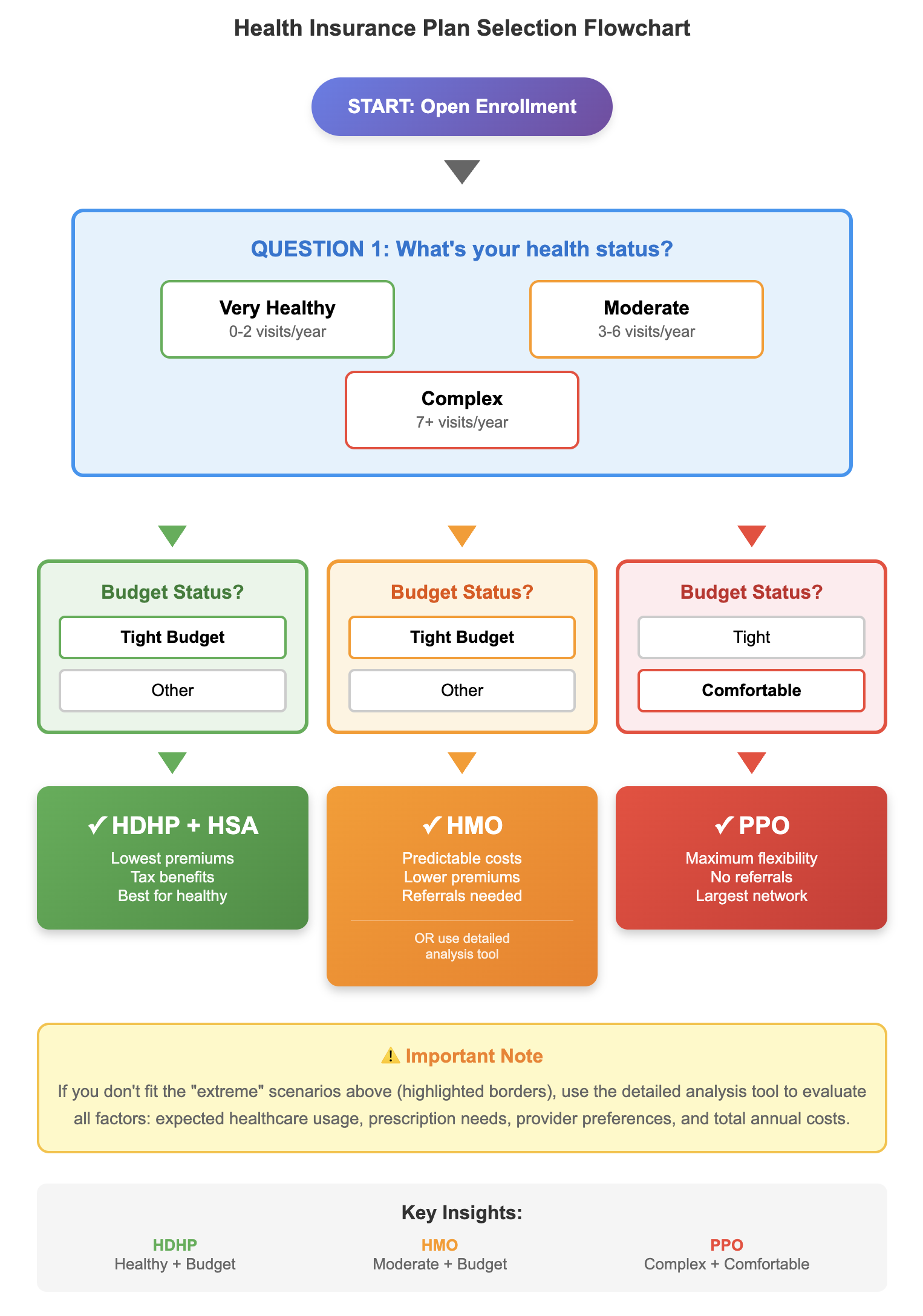

- Tools & Tips: Health Insurance Plan Type Helper

- Market Overview

-

Walmart 401(k) Investment Options: Complete Fund Guide 2025

The Walmart 401(k) Plan continues to be one of the largest employer-sponsored retirement programs in the country. This 2025 guide distills the latest filing details and helps Walmart associates make informed choices across the Walmart 401k investment options, Walmart 401k funds, and broader Walmart retirement plan investments lineup.

-

Maximize Your Walmart 401(k) Employer Match: Complete 2025 Guide

Everything Walmart associates need in 2025 to capture the plan’s full 6% employer match, automate smart contribution strategies, and stay on track for millionaire-level retirement savings.

-

How to Navigate Medicare Maze

- Latest in Retirement Savings & Personal Finance: Shutdown Showdown,Turning Fulough into an Opportunity,Subprime Auto Loan Trouble

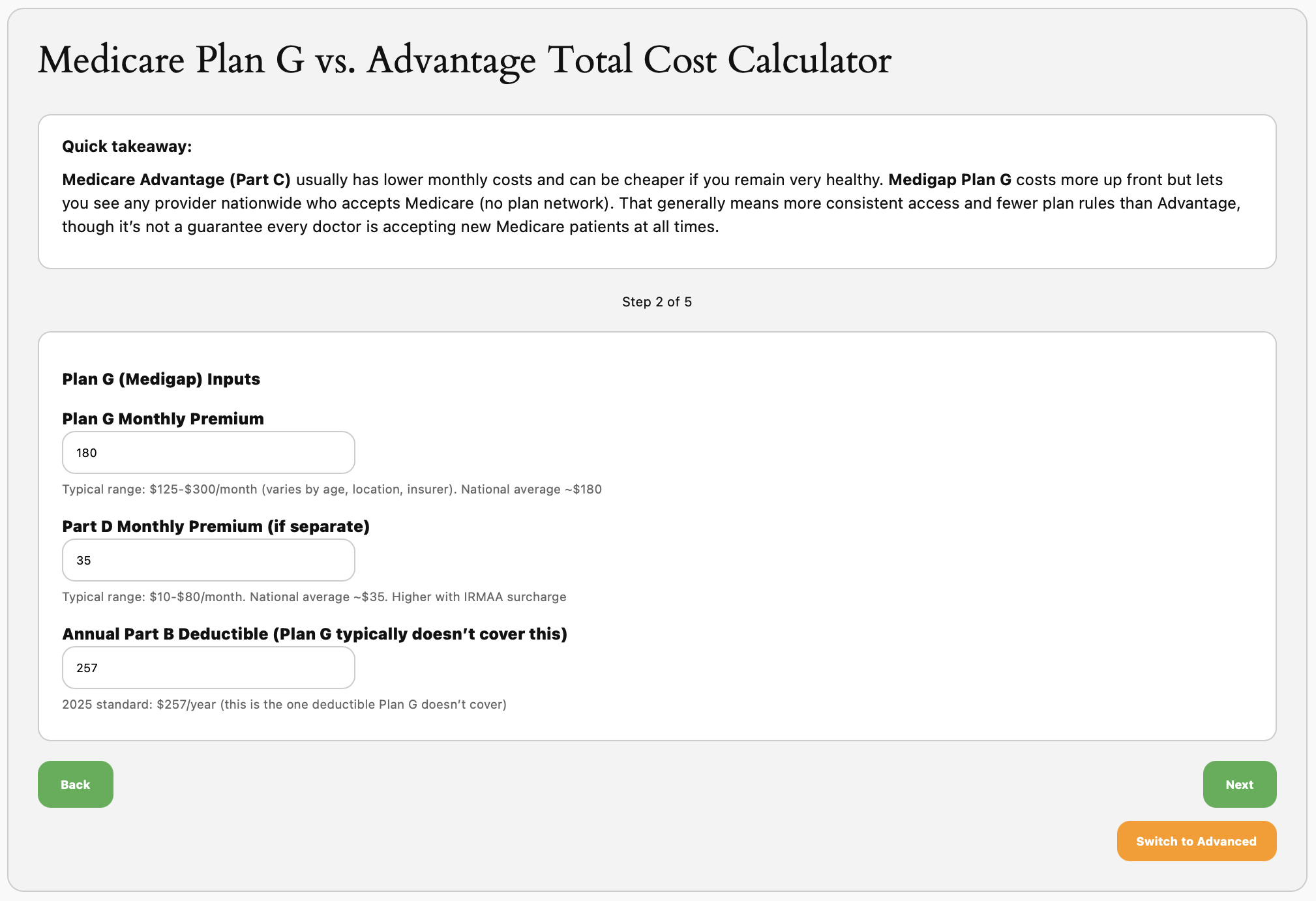

- Traditional Medicare (Medigap) vs. Medicare Advantage

- Tools & Tips: Medicare Medigap vs. Medicare Advantage Total Cost Calculator

- Market Overview

-

Traditional Medicare (Medigap) vs. Medicare Advantage

We compare Medigap vs. Medicare Advantage and hopefully give a clear guidance for people to weigh pros and cons between them.

-

Microsoft Roth 401(k) & Mega Backdoor Roth Strategy Guide 2025

Microsoft Corporation’s Savings Plus 401(k) Plan gives you every tool needed to build tax-free retirement wealth: Roth salary deferrals, generous after-tax capacity, and instant in-plan conversions. This guide explains how to harness those features in 2025 so you can graduate from “traditional saver” to future tax-free millionaire. ✅ Available: Microsoft Roth 401(k) Pre-tax and Roth deferrals run through the same Fidelity portal. Switching your paycheck elections to Roth lets you pay taxes now while locking in tax-free qualified withdrawals later. Catch-up contributions ($7,500) can be directed to Roth as well. ✅ Available: Mega Backdoor Roth via After-Tax Contributions Microsoft supports sizable after-tax contributions (historically up to $34,500) plus in-plan Roth conversions. That combination satisfies the two critical requirements for executing a mega backdoor Roth inside Fidelity NetBenefits. Roth 401(k) Benefits for Microsoft Employees The Roth 401(k) bucket grows tax-free and distributes tax-free as long as you hold the account for five years and reach age 59½. Because Microsoft allows you to defer up to 65% of eligible pay (subject to the IRS $23,000 limit, or $30,500 with catch-up), high earners can rapidly build Roth balances while still collecting the full employer match. Mega Backdoor Roth Playbook Microsoft’s plan checks every box for the mega backdoor Roth (MBDR) tactic: after-tax contributions, in-plan conversions, and a high overall contribution ceiling (IRS Section 415(c) limit of $69,000, or $76,500 with catch-up). By filling the after-tax bucket and immediately converting it to Roth, you can move tens of thousands of dollars into tax-free growth every year. Interactive Roth vs. Traditional Calculator .available-feature { background: #f3f9ff; border-left: 4px solid #1966d2; padding: 1.25rem 1.5rem; border-radius: 0.75rem; margin: 1.5rem 0; } .strategy-comparison { background: #f7fbff; border: 1px solid #d4e5ff; border-radius: 0.75rem; padding: 1.25rem 1.75rem; margin: 1.5rem 0; } .wp-block-group.roth-calculator, .wp-block-group.mbdr-calculator { background: #f3f3f3; border: 1px solid #cccccc; border-radius: 0.9rem; padding: 1.5rem; margin: 2rem auto; max-width: 60%; } .wp-block-group.roth-calculator h3, .wp-block-group.mbdr-calculator h3 { margin-top: 0; color: #143c7d; } .calculator-inputs { display: flex; flex-direction: column; gap: 1rem; margin-bottom: 1.25rem; } .calculator-inputs label { display: flex; flex-direction: column; font-weight: 700; color: #102a53; } .calculator-inputs input, .calculator-inputs select { margin-top: 0.5rem; padding: 0.65rem 0.8rem; border-radius: 0.6rem; border: 1px solid #b8c7e3; font-size: 1rem; background: #ffffff; max-width: 18rem; } .calculator-inputs button { align-self: flex-start; padding: 0.85rem 1.4rem; border: none; border-radius: 0.6rem; background: #4CAF50; color: #ffffff; font-weight: 700; cursor: pointer; transition: transform 0.15s ease, box-shadow 0.15s ease; } .calculator-inputs button:hover { transform: translateY(-1px); box-shadow: 0 8px 16px rgba(76, 175, 80, 0.25); } .calculator-results { background: #ffffff; border-radius: 0.75rem; border: 1px solid #d5deef; padding: 1.1rem; color: #0f2557; } .calculator-results p { margin: 0.5rem 0; } .calculator-results ul { padding-left: 1.25rem; margin: 0.5rem 0; } .calculator-note { font-size: 0.9rem; color: #374f7a; margin-top: 0.75rem; } @media (max-width: 960px) { .wp-block-group.roth-calculator, .wp-block-group.mbdr-calculator { max-width: 90%; } } @media (max-width: 640px) { .calculator-inputs input, .calculator-inputs select { max-width: 100%; } } Roth vs. Traditional 401(k) Calculator for Microsoft Employees Current Age Household Income ($) Current Tax Bracket 12%22%24%32%35%37% Expected Retirement Tax Bracket 12%22%24%32% Annual Contribution ($) Expected Annual Return (%) Compare Roth vs. Traditional Assumes retirement at age 65 and constant contribution/return rates. Adjust inputs to reflect your tax outlook. const IRS_DEFERRAL_LIMIT = 23000; const CATCH_UP_LIMIT = 7500; const IRS_415C_LIMIT = 69000; function parseCurrencyInput(rawValue) { if (rawValue === undefined || rawValue === null) { return 0; } const cleaned = rawValue.toString().replace(/,/g, ”).trim(); const numeric = Number(cleaned); if (Number.isNaN(numeric)) { return 0; } return numeric; } function formatCurrency(value) { return ‘$’ + value.toLocaleString(‘en-US’, { minimumFractionDigits: 2, maximumFractionDigits: 2 }); } function formatCompactCurrency(value) { return ‘$’ + value.toLocaleString(‘en-US’, { maximumFractionDigits: 2 }); } function syncCurrencyInput(id) { const el = document.getElementById(id); if (!el) { return; } el.value = parseCurrencyInput(el.value).toLocaleString(‘en-US’, { maximumFractionDigits: 0 }); } function calculateFutureValue(contribution, years, rate) { if (rate === 0) { return contribution * years; } const futureFactor = Math.pow(1 + rate, years) – 1; return contribution * futureFactor / rate; } function calculateRothComparison() { syncCurrencyInput(‘rcIncome’); syncCurrencyInput(‘rcContribution’); const age = Number(document.getElementById(‘rcCurrentAge’).value); const income = parseCurrencyInput(document.getElementById(‘rcIncome’).value); const currentTax = Number(document.getElementById(‘rcCurrentTax’).value); const retirementTax = Number(document.getElementById(‘rcRetirementTax’).value); const annualContribution = parseCurrencyInput(document.getElementById(‘rcContribution’).value); const annualReturnPercent = Number(document.getElementById(‘rcReturn’).value); const output = document.getElementById(‘rcResults’); if (age < 18 || annualContribution

-

Microsoft 401(k): Unlock Every Match Dollar and Compound Your Contribution

The Microsoft Corporation Savings Plus 401(k) Plan is a wealth-building powerhouse. With immediate vesting, broad Roth and after-tax flexibility, and a generous employer match, disciplined saving today can realistically put you on the path to 401(k) millionaire status. This 2025 playbook shows you exactly how to capture every “free money” dollar Microsoft offers and keep your retirement trajectory compounding upward. Microsoft’s 2025 Employer Match Snapshot Core Microsoft, LinkedIn, GitHub, ZeniMax, and other subsidiaries: Microsoft contributes $0.50 for every $1 you defer on a pre-tax or Roth basis, matching your salary deferrals all the way up to the IRS elective deferral limit (currently $23,000). When you contribute the full limit, Microsoft adds $11,500 in employer dollars. inXile Entertainment & Double Fine Productions: These studios receive $0.25 per $1 deferred on pre-tax or Roth contributions, up to that same IRS limit. Contributing $23,000 generates a maximum $5,750 match. Immediate vesting & no safe harbor designation: Every match dollar is yours instantly. Because the plan isn’t classified as safe harbor, stay mindful of annual ADP/ACP testing—front-load savings if you are a highly compensated employee. Contribution Limits, Catch-Up Rules, and Mega Backdoor Potential Microsoft lets you combine pre-tax, Roth, and after-tax percentages up to 65% of eligible pay each paycheck. The latest published IRS elective deferral limit remains $23,000, with an additional $7,500 catch-up allowance for employees turning age 50 by year-end. Catch-up dollars are not matched, but they still reduce taxable income (pre-tax) or can be directed to Roth for future tax-free growth. After maximizing pre-tax and Roth contributions, you can push as much as $34,500 (per 2024 filing) into after-tax contributions. Pair those dollars with Microsoft’s in-plan Roth conversion feature—or roll after-tax balances to a Roth IRA if you exit—to execute the mega backdoor Roth strategy and grow more money tax-free. Need more investment choice? Fidelity BrokerageLink opens a self-directed brokerage window alongside the default BlackRock LifePath Index CITs, Vanguard index trusts, and Fidelity pooled funds. Just remember: Microsoft only matches what you contribute; the sooner you hit the match threshold, the faster every investment option can compound. .key-takeaways { background: #f4f8ff; border-left: 4px solid #1846a3; padding: 1.25rem 1.5rem; border-radius: 0.75rem; margin: 1.5rem 0; } .highlight-box { background: linear-gradient(135deg, #eef4ff 0%, #f7fbff 100%); border-left: 4px solid #2560c4; padding: 1.5rem; border-radius: 0.75rem; box-shadow: 0 10px 30px rgba(37, 96, 196, 0.12); } .wp-block-group.match-calculator, .wp-block-group.projection-calculator { background: #f3f3f3; border: 1px solid #cccccc; border-radius: 0.9rem; padding: 1.5rem; margin: 2rem auto; max-width: 60%; } .wp-block-group.match-calculator h3, .wp-block-group.projection-calculator h3 { margin-top: 0; color: #143c7d; } .calculator-inputs { display: flex; flex-direction: column; gap: 1rem; margin-bottom: 1.25rem; } .calculator-inputs label { display: flex; flex-direction: column; font-weight: 700; color: #102a53; } .calculator-inputs input, .calculator-inputs select { margin-top: 0.5rem; padding: 0.65rem 0.8rem; border-radius: 0.6rem; border: 1px solid #b8c7e3; font-size: 1rem; background: #ffffff; max-width: 18rem; } .calculator-inputs button { align-self: flex-start; padding: 0.85rem 1.4rem; border: none; border-radius: 0.6rem; background: #4CAF50; color: #ffffff; font-weight: 700; cursor: pointer; transition: transform 0.15s ease, box-shadow 0.15s ease; } .calculator-inputs button:hover { transform: translateY(-1px); box-shadow: 0 8px 16px rgba(76, 175, 80, 0.25); } .calculator-results { background: #ffffff; border-radius: 0.75rem; border: 1px solid #d5deef; padding: 1.1rem; color: #0f2557; } .calculator-results p { margin: 0.5rem 0; } .calculator-results ul { padding-left: 1.25rem; margin: 0.5rem 0; } .calculator-note { font-size: 0.9rem; color: #374f7a; margin-top: 0.75rem; } .action-list { list-style: decimal; padding-left: 1.5rem; line-height: 1.6; } @media (max-width: 960px) { .wp-block-group.match-calculator, .wp-block-group.projection-calculator { max-width: 90%; } } @media (max-width: 640px) { .calculator-inputs input, .calculator-inputs select { max-width: 100%; } } Interactive Microsoft 401(k) Match Calculator 2025 Microsoft Match Maximizer Enter Your Annual Salary ($) Select Pay Frequency Bi-weekly (26 pays)Semi-monthly (24 pays)Monthly (12 pays) Business Unit Core Microsoft, LinkedIn, GitHub, ZeniMax, etc.inXile & Double Fine studios Age 50+ Catch-Up? NoYes (adds $7,500 employee-only) Calculate My Match The IRS has not yet released a 2025 elective deferral limit. Calculations use the most recent published figures ($23,000 plus $7,500 catch-up) so you can plan contributions now and adjust quickly when the IRS updates guidance. const IRS_LIMIT = 23000; const CATCH_UP_LIMIT = 7500; const PAY_PERCENT_CAP = 0.65; function parseCurrencyInput(rawValue) { if (rawValue === undefined || rawValue === null) { return 0; } const cleaned = rawValue.toString().replace(/,/g, ”).trim(); const numeric = Number(cleaned); if (Number.isNaN(numeric)) { return 0; } return numeric; } function syncCurrencyInput(id) { const element = document.getElementById(id); if (!element) { return; } const numeric = parseCurrencyInput(element.value); element.value = formatCurrency(numeric).replace(‘$’, ”); } function getCurrencyInput(id) { const element = document.getElementById(id); if (!element) { return 0; } return parseCurrencyInput(element.value); } function formatCurrency(value) { const formatted = value.toLocaleString(‘en-US’, { minimumFractionDigits: 2, maximumFractionDigits: 2 }); return ‘$’ + formatted; } function formatPercent(value) { return value.toFixed(2) + ‘%’; } function getBusinessProfile(unit) { if (unit === ‘inxile’) { return { label: ‘inXile & Double Fine’, matchRate: 0.25, eligibleFraction: 1.0 }; } return { label: ‘Core Microsoft businesses’, matchRate: 0.50, eligibleFraction: 1.0 }; } function calculateMicrosoftMatch() { syncCurrencyInput(‘matchSalary’); const salary = getCurrencyInput(‘matchSalary’); const periodField = document.getElementById(‘matchPayPeriods’); const periodValue = Number(periodField.value); let payPeriods = periodValue; if (Number.isNaN(periodValue)) { payPeriods = 26; } const unit = document.getElementById(‘matchBusinessUnit’).value; const catchUpChoice = document.getElementById(‘matchCatchUp’).value; const resultsContainer = document.getElementById(‘matchResults’); if (salary salary) { employeeContributionCap = salary; } const matchEligibleEmployeeCap = IRS_LIMIT * profile.eligibleFraction; let attainableEmployeeForMatch = matchEligibleEmployeeCap; if (employeeContributionCap < attainableEmployeeForMatch) { attainableEmployeeForMatch = employeeContributionCap; } if (salary < attainableEmployeeForMatch) { attainableEmployeeForMatch = salary; } const employerMatchEarned = attainableEmployeeForMatch * profile.matchRate; const totalAnnualRetirement = attainableEmployeeForMatch + employerMatchEarned; const perPayEmployee = attainableEmployeeForMatch / payPeriods; const deferralPercent = (attainableEmployeeForMatch / salary) * 100; const requestedFullMatch = attainableEmployeeForMatch >= matchEligibleEmployeeCap; const theoreticalEmployerMatch = matchEligibleEmployeeCap * profile.matchRate; const theoreticalTotal = matchEligibleEmployeeCap + theoreticalEmployerMatch; let matchStatusLine = ‘

- You are on track to capture the full stated employer match when you contribute this amount.

‘; if (!requestedFullMatch) { const shortfall = matchEligibleEmployeeCap – attainableEmployeeForMatch; const formattedShortfall = shortfall.toLocaleString(‘en-US’, { minimumFractionDigits: 2, maximumFractionDigits: 2 }); matchStatusLine = ‘

- You will capture all match that your compensation and plan limits allow, but you fall $’ + formattedShortfall + ‘ short of the theoretical full-match contribution. Consider bonuses, earlier contributions, or catch-up adjustments to close the gap.

‘; } const additionalEmployeeCapacity = employeeContributionCap – attainableEmployeeForMatch; let extraSavingsNote = ‘You still have room to add ‘ + formatCurrency(additionalEmployeeCapacity) + ‘ before hitting the IRS elective deferral limit that earns matching dollars.’; if (additionalEmployeeCapacity 0) { compoundBalance = balance * Math.pow(1 + monthlyRate, months); const growthFactor = Math.pow(1 + monthlyRate, months) – 1; const contributionGrowth = monthlyContribution * growthFactor / monthlyRate; return compoundBalance + contributionGrowth; } const straightContribution = monthlyContribution * months; return compoundBalance + straightContribution; } function calculateMicrosoftProjection() { syncCurrencyInput(‘projectionSalary’); syncCurrencyInput(‘projectionBalance’); const salaryField = document.getElementById(‘projectionSalary’); const balanceField = document.getElementById(‘projectionBalance’); const returnField = document.getElementById(‘projectionReturn’); const yearsField = document.getElementById(‘projectionYears’); const catchUpField = document.getElementById(‘projectionCatchUp’); const output = document.getElementById(‘projectionResults’); const salaryValue = getCurrencyInput(‘projectionSalary’); const balanceValue = getCurrencyInput(‘projectionBalance’); const returnValue = Number(returnField.value); const yearsValue = Number(yearsField.value); if (Number.isNaN(salaryValue) || salaryValue salaryValue) { maximumEmployeeContribution = salaryValue; } const matchEligibleEmployeeCap = IRS_LIMIT; let employeeForMatch = matchEligibleEmployeeCap; if (maximumEmployeeContribution < employeeForMatch) { employeeForMatch = maximumEmployeeContribution; } const projectionMatchRate = 0.50; const matchAtEmployeeForMatch = employeeForMatch * projectionMatchRate; const totalForMatchStrategy = employeeForMatch + matchAtEmployeeForMatch; const matchAtMax = Math.min(matchEligibleEmployeeCap, maximumEmployeeContribution) * projectionMatchRate; const totalForMaxStrategy = maximumEmployeeContribution + matchAtMax; const annualReturnRate = returnValue / 100; const monthlyRate = annualReturnRate / 12; const totalMonths = yearsValue * 12; const monthlyContributionMatch = totalForMatchStrategy / 12; const monthlyContributionMax = totalForMaxStrategy / 12; const futureMatchStrategy = futureValue(balanceValue, monthlyContributionMatch, monthlyRate, totalMonths); const futureMaxStrategy = futureValue(balanceValue, monthlyContributionMax, monthlyRate, totalMonths); const millionaireThreshold = 1000000; let millionaireMessage = ‘Staying disciplined with the max strategy keeps you ‘ + formatCurrency(futureMaxStrategy – millionaireThreshold) + ‘ beyond the millionaire mark in ‘ + yearsValue + ‘ years.’; if (futureMaxStrategy < millionaireThreshold) { const shortfall = millionaireThreshold – futureMaxStrategy; millionaireMessage = ‘Increase contributions or adjust returns—the max strategy finishes ‘ + formatCurrency(shortfall) + ‘ short of the millionaire milestone over ‘ + yearsValue + ‘ years.’; } output.innerHTML = ‘ Annual employee cap considered: ‘ + formatCurrency(maximumEmployeeContribution) + ‘ (subject to 65% of pay). ‘ + ‘

- ‘ +

‘

- Match-only strategy (contribute just enough to earn Microsoft’s full 50% match): ‘ + formatCurrency(totalForMatchStrategy) + ‘ added yearly → projected balance: ‘ + formatCurrency(futureMatchStrategy) + ‘. ‘ + ‘

- Max deferral strategy (fill the IRS + catch-up window): ‘ + formatCurrency(totalForMaxStrategy) + ‘ added yearly → projected balance: ‘ + formatCurrency(futureMaxStrategy) + ‘. ‘ + ‘

‘ + ‘ ‘ + millionaireMessage + ‘ ‘ + ‘ Once you fill the IRS bucket, remember that Microsoft permits substantial after-tax contributions. Converting those after-tax dollars to Roth inside the plan can accelerate your millionaire timeline. ‘; } document.addEventListener(‘DOMContentLoaded’, function () { calculateMicrosoftMatch(); calculateMicrosoftProjection(); }); Action Plan: Capture the Match and Keep Compounding

- Auto-escalate contributions today. Log into Fidelity NetBenefits, set your deferral high enough to hit the match threshold early in the year, and use the 65% paycheck cap to catch up after bonuses.

- Map your Roth and after-tax mix. Use pre-tax deferrals if you need the tax deduction; otherwise, build Roth and after-tax balances for tax-free future withdrawals. Coordinate with the Microsoft Roth 401(k) strategy guide to execute mega backdoor conversions.

- Rebalance quarterly. Microsoft’s default BlackRock LifePath Index funds are strong set-it-and-forget-it options. If you leverage BrokerageLink, create a rebalancing reminder to stay diversified.

- Track vesting and compliance testing. You are 100% vested immediately, but highly compensated employees should monitor year-end refunds and adjust early if ADP/ACP testing historically impacts your team.

- Schedule an annual check-in. Each fall, revisit salary increases, IRS limit updates, and match formulas so your 2026 contributions start at optimal levels on January 1.

Need Help or Have Plan Questions? Plan administrator: 401(k) Administrative Committee, One Microsoft Way, Redmond, WA 90852-6399, phone 425-882-8080. Recordkeeper & trustee: Fidelity Investments Institutional (service codes 37, 71, 64, 51, 65). Log into Fidelity NetBenefits or call the participant service center to adjust deferrals, launch BrokerageLink, or confirm after-tax conversion steps. If you have unique match rules (for example, you sit within inXile or Double Fine), confirm your unit’s match percentage in the NetBenefits portal before finalizing elections. When in doubt, escalate through Microsoft’s HR Support portal for written confirmation. Stay Proactive in 2025 The Savings Plus 401(k) is designed for builders: immediate vesting, generous match potential, and every tax-advantaged contribution type under one roof. Automate contributions now, revisit the calculators each time your compensation changes, and you’ll keep Microsoft’s “free money” working overtime toward your long-term financial independence. { “@context”: “https://schema.org”, “@type”: “FinancialProduct”, “name”: “Microsoft Corporation Savings Plus 401(k) Plan Employer Match Guide”, “description”: “Step-by-step 2025 guide for Microsoft employees to maximize 401(k) contributions, employer match dollars, and mega backdoor Roth strategies.”, “provider”: { “@type”: “Organization”, “name”: “Microsoft Corporation”, “url”: “https://www.microsoft.com” }, “areaServed”: { “@type”: “AdministrativeArea”, “name”: “United States” }, “financialServiceType”: “401(k) employer match optimization”, “audience”: { “@type”: “Audience”, “audienceType”: “Microsoft employees” }, “offers”: { “@type”: “Offer”, “price”: “0”, “priceCurrency”: “USD”, “availability”: “https://schema.org/InStock” } }

-

October 2025 MyPlanIQ Portfolio Update

- Why Long-Term Investors Should Embrace Technology: Tech Investment Growth, Risks and Opportunities

- Some Selective Tech ETFs

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

How Much Cash Do You Need?

- Latest in Retirement Savings & Personal Finance: Stocks Most Expensive,Low Number of Job Postings,Naming Your Baby $30K A Pop

- How Much Cash Do You Need?

- Tools & Tips: Emergency Income Checker

- Market Overview

-

HSA: One of The Biggest Tax Break You Shouldn’t Ignore

- Latest in Retirement Savings & Personal Finance: What Fed Rate Cut Means for You? Surge in Electricity Prices

- Health Savings Account (HSA): One of The Biggest Tax Break You Shouldn’t Ignore

- Tools & Tips: HSA Savings Calculator

- Market Overview

-

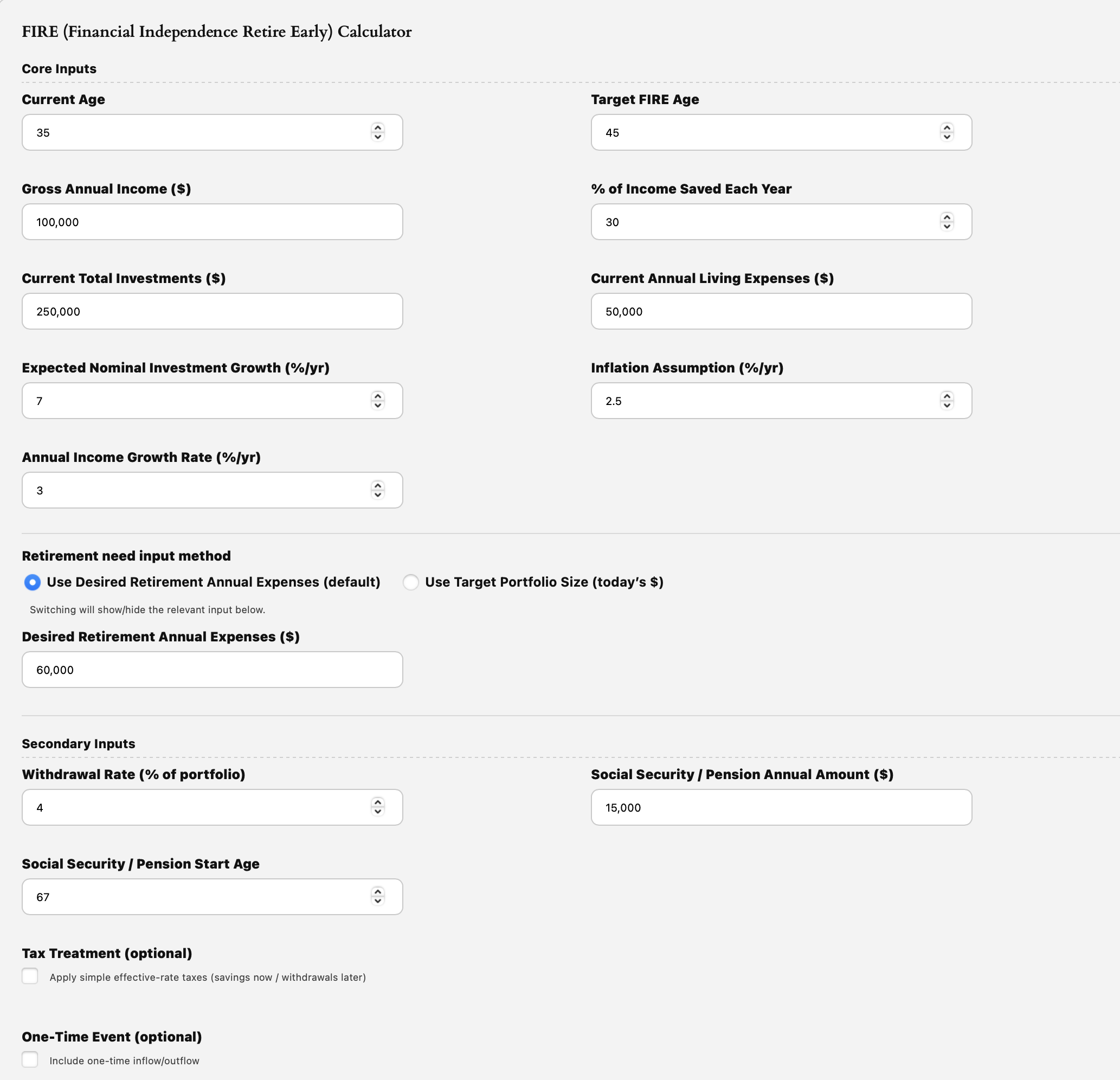

Good Time to FIRE (Financial Independence Retire Early)?

- Latest in Retirement Savings & Personal Finance: Fed to Cut Rate, AI Big Spend, Oracle of Oracle

- Good Time to FIRE (Financial Independence Retire Early)?

- Tools & Tips: FIRE (Financial Independence Retire Early) Calculator

- Market Overview

-

When the Fed Cuts Rates, What Really Happens to Stocks?

- Latest in Retirement Savings & Personal Finance: Job Growth Slowed, Gen Z Dipped into Retirement Savings, Best S&P 500 Earnings in Four Years

- When the Fed Cuts Rates, What Really Happens to Stocks?

- Tools & Tips: Total Compensation Calculator

- Market Overview

-

Gold Shines as a Store of Value

- Latest in Retirement Savings & Personal Finance: Rise in U.S. Bankruptcies, Surging Long-Term Bond Yields Worldwide

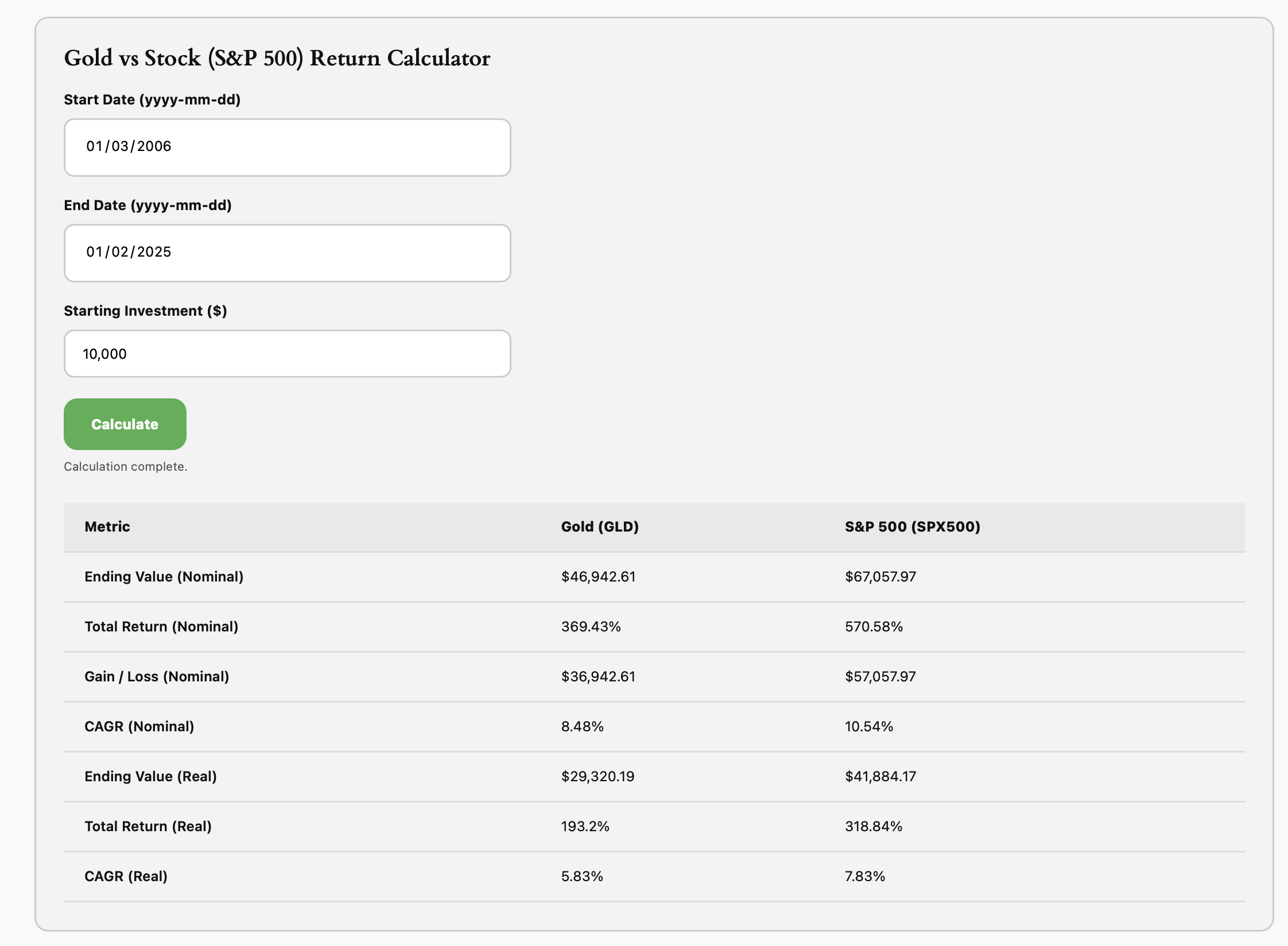

- Gold Shines as a Store of Value

- Tools & Tips: Gold vs Stock Return Calculator

- Market Overview

-

September 2025 MyPlanIQ Portfolio Update

- Stock and Bond Returns in the Next Decade

- Conservative Allocation Funds Review

- Economic & Market Indicators

- Model Portfolios

- Funds to Watch

- Market Overview

-

Saving and Investing for College in a World of Runaway Tuition

- Latest in Retirement Savings & Personal Finance: Runaway College Tuitions, Vanguard Now Recommends 30% Stocks 70% Bonds

- Social Security at Risk: Saving and Investing for College in a World of Runaway Tuition

- Tools & Tips: 529 Plan Tax Savings Calculator

- Market Overview

-

Home Rent vs. Buy: That’s A Great Question

- Latest in Retirement Savings & Personal Finance: Social Security COLA Expected to 2.7%, Consumers Hit 70% Tariff by October

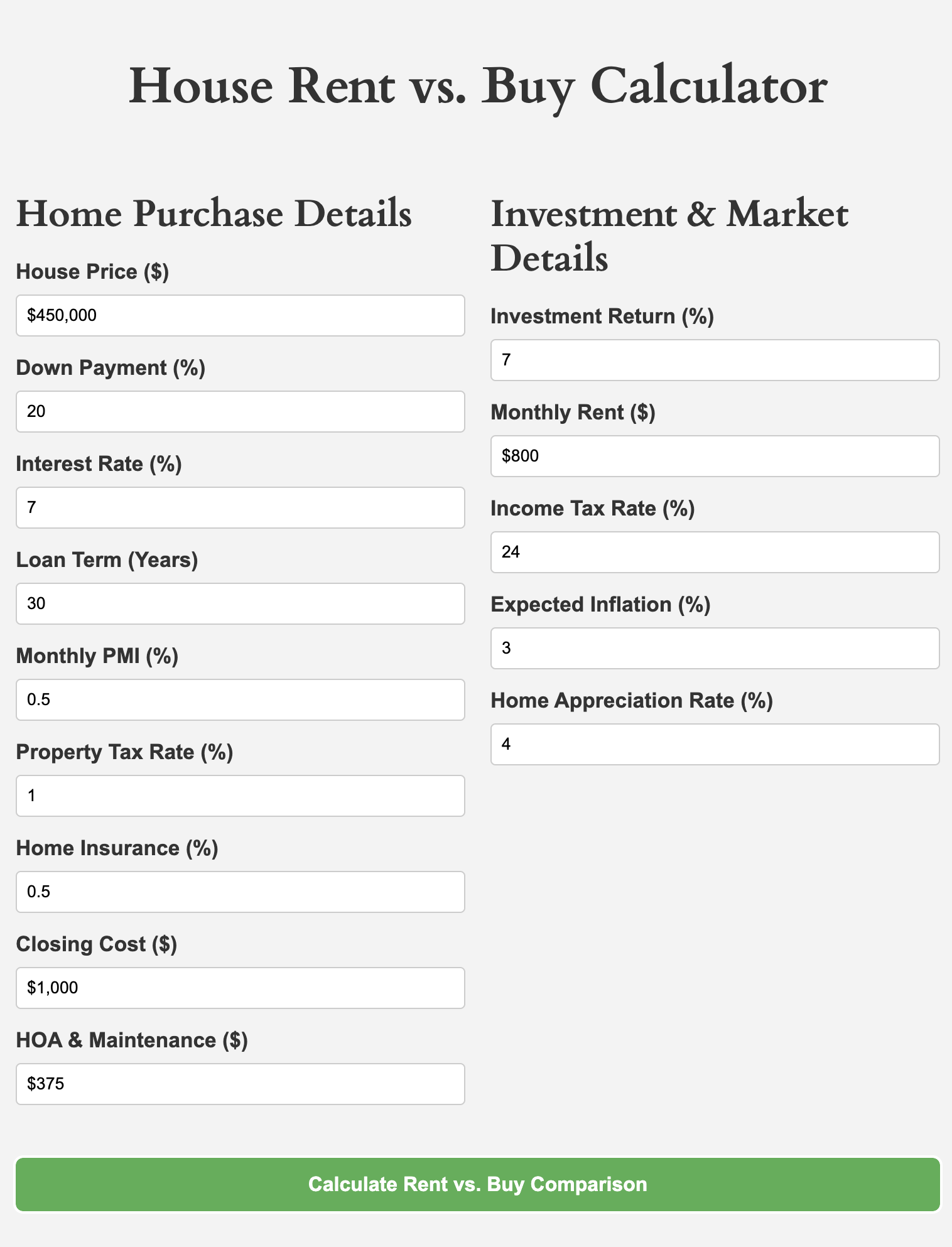

- Social Security at Risk: Home Rent vs. Buy: That’s A Great Question

- Tools & Tips: Home Rent vs. Buy Calculator

- Market Overview